In a report released by Access Economics today, it expects retail sales to grow by only 1.3 percent this financial year, sounding the worst period for retail spending in two decades. But, on a positive note, it expects a rebound next year.

David Rumbensm, a partner with Deloitte Access Economics said “People are more cautious and saving more.”

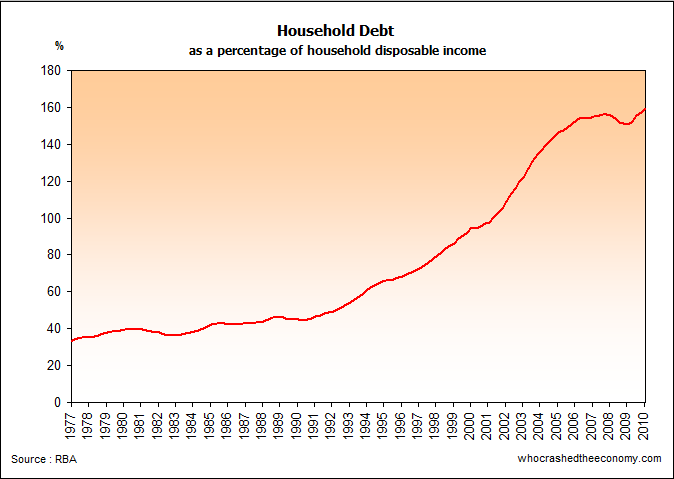

ABS data shows household savings have rapidly sprung back to levels not seen in 25 years after a decade when the household consumption fired along on the expansion of credit. The unsustainable surge in house prices and the wealth effect helped the retail sector along nicely. But pushed under the carpet is the white elephant in Australian lounge rooms – excessive debt levels, gradually accumulated over the last two decades. 90 percent of that debt belongs to residential housing.

While current interest rates are some of the lowest in decades,

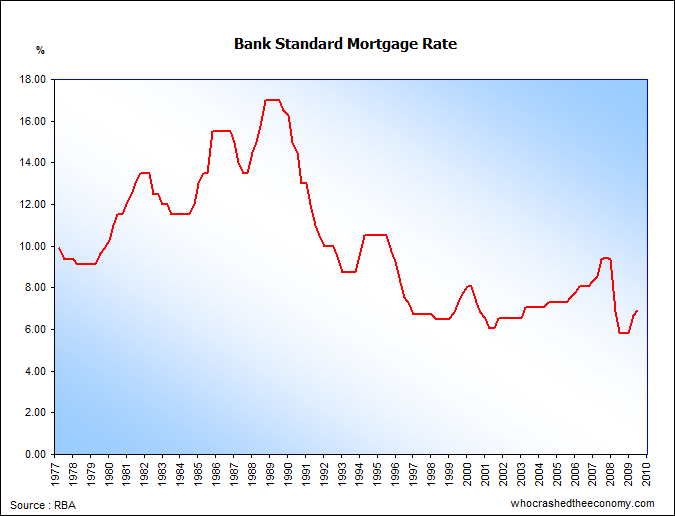

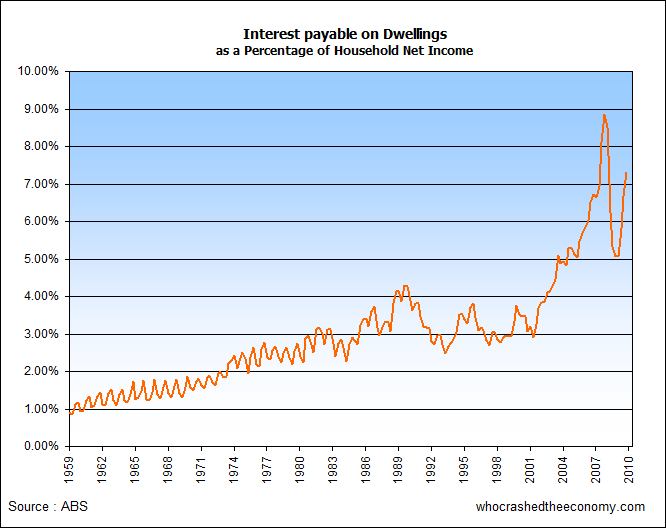

Our extremely high debt levels have seen mortgage payments blow out to record levels. While the Boomer’s remember the 17 percent interest rates of the late 1980s, just prior to the GFC the aggregate Australian household was spending double the amount on mortgage interest payments than when rates were 17 percent. And they thought they had it tough.

David Rumbens says “In part, it’s the lift in interest rates that we saw last year that has both cut into incomes and cut confidence.” He believes we can expect another rate rise in the coming months. With the level of debt we have today, a 25 basis point rise in official interest rates has a greater effect than in the 1990s. For this reason, some believe the RBA is resorting to warning of impending rate rises to help cool household’s addiction to debt, rather than inflict the pain of actually carrying through with it.

Only today, credit ratings agency Fitch was forced to revise its estimates of pending mortgage defaults up as their model used data on loan performance between 1980 and 2000 when debt levels were much lower. “These figures show a substantial shift in the indebtedness of Australian borrowers, who are now significantly more sensitive to moves in interest rates than they were 20 years ago,” Fitch said. “For this reason, Fitch believes any downturn could be significantly worse than the recession of 1991, on which the current mortgage default criteria is based.”

While this excessive household debt level, worldwide, was the cause of the GFC, our government decided in its wisdom to prop up our unsustainable economy. Of course, proping up an unsustainable economy means when the stimulus is removed, the economy once again collapses as the root of the problem is not addressed. In fact, as you can see in the graph of household debt above, Australian’s started reducing their reliance on debt after the GFC, only for the government to provide free money to help encourage more accumulation of it via a period of fast house price growth.

With the effects of the stimulus running out, Australian’s are now once again saving like never before in a bid to keep their heads above water and pay down the crippling debt levels. House prices are falling, and the negative wealth effect means consumer confidence is falling.

“In part, it’s house prices having peaked and now starting to turn down has also cut confidence and willingness to spend.” said David Rumbens.

Deloitte Access Economics predicts that household savings will start to level out, and that a jobs and wage growth will help fuel a rebound in consumer confidence and retail sales next financial year.

Have your say. Is this possible?

» First home buyer defaults more likely: Fitch – The Age, 8th June 2011.

» Australia Retail Sales to Increase From Two-Decade Low, Access Report Says – Bloomberg, 7th June 2011.

» Retail sales ‘to bounce back next year’ – The ABC, 8th June 2011.

» Retail sales expected to pick up after horror year: Access Economics – Smart Company, 8th June 2011.

» Christmas retail figures shaping up to be the worst since the early 90′s – Who Crashed the Economy, 23rd December 2010.

» Time to pick and choose: Housing or Jobs – Who Crashed the Economy, 21st March 2009.

According to accounting identities, it’s not possible for the household sector to save without the creation of credit (debt) in the business sector or the Government sector.

If the Government is heading for debt balance, business is not creating debt, and the household sector is saving, then the saving is not real saving it’s the repayment of debt.

The repayment of debt reduces the money supply.

A strange possibility maybe… the creation of a USD debt (credit) also creates a USD deposit which is used to purchase an AUD deposit which is created by an AUD debt (credit) and the security for the USD debt (credit) is the AUD deposit and the security for the AUD debt (credit) is the USD deposit.

Under that scenerio, a flow of interest payments moves from Australia to the USA becuase of the interest rate differential (carry trade).

It’s possible (and I’m uncertain about this) that the big jump in Australian Bank deposits… loosely termed ‘household saving’ is ‘Hot Money’ exploiting the carry trade.

Sometimes a category like ‘Household saving’ is a catch all for all the accounting things that are not defined elsewhere.

Caveat emptor

I’ll wait a see when the bounce back in retail spending comes, it was supposed to come last year, and the year before that, and the one before that.

Increase in savings, maybe, I don’t know. What I know is more people are tapping into their SuperAnnuation (for what ever reason), and allocating much less money in SuperAnnuation. On a personal level, I’m seeing more credit cards and EFTPOS cards being declined in supermarket checkouts, petrol stations, and restaurants. There is a feeling of much less money in peoples hands, and a bit more stress and anxiety. Savings would entail people appearing as bit stronger and calmer. I guess there are a few people with huge bank accounts, and many on the borderline (maybe they’re a minority or don’t count for much).

The question, “who crashed the economy?”, is becoming a rhetorical one.

“Deloitte Access Economics predicts that household savings will start to level out, and that a jobs and wage growth will help fuel a rebound in consumer confidence and retail sales next financial year. ”

Yoda say – Access economics is actually here to referring to Vietnam and not Australia.

Australian savings will fall as we continue to pay interest to banksters and new fantastic taxes that will save the world. We will loose more jobs overseas because of globalisation and the wage growth will only be in the public sector as profit is not a concern. Private sector in depression with the retail discretionary shops at the forefront.

Yoda say – Lets reduce government, lower taxes bigtime and allow business to flourish with out the leech sucking the life out of it. Hell, lets make business that looks after the environment tax free.

Excellent article – one of the best I’ve seen here. It’s about time the banks were exposed for what they are, sellers of debt enslavement. I mean look at the ridiculous price of housing and the spruikers tell us its going to double again from here, and how are we supposed to pay for that? More debt from the banks of course. The banks will never admit housing is in a bubble for as soon as they admit it they know the whole ponzi comes crashing down. Oh well, I guess we just wait. The insanity can’t go on for much longer and soon we’ll see the market collapse under its own weight. A rapid fall in consumer spending is a classic symptom of an economic bubble bursting.

Worried Observer

Australian Housing Affordability Blog

Breaking news from Yoda – The Bilderbergs are meeting in St Moritz Switzerland this Saturday. There may be responsible for crashing the economy according to Alex Jones and other liberty advocates.

There are rumours of a Bilderberg Protest in Switzerland that will try and persuade the global elite to stop destoying our wealth by global taxes etc.

Yoda not attend as Yoda space ship got no fuel as carbon price limit use, international travel taxes etc. Yoda watch protest on You tube instead.

Advice given to Yoda last night at RE Agent investor night.

TAKE YOUR HOUSE OFF THE MARKET IF YOU DON’T HAVE TO SELL !!!!! Why? Are there more sellers ATM? Yoda think RE Agent up creek with no paddle and is desperate to avoid imploding real estate market.

Retail industry is not going to recover until the consumer gets out of debt. With record debt on the cards and mortgage defaults at a record high I dont see retail recovering for a while. Plus the govt cant spend it way out of this one again. Now that China is starting to deflate at a rapid pace that will prolong any type of recovery. Australia GFC on the way. I am waiting to read the banks going back to the govt for money or guarantees soon.

http://www.couriermail.com.au/news/breaking-news/new-research-shows-australian-home-owners-among-the-worlds-most-indebted/story-e6freonx-1226072347372

This is interesting

Credit creates deposits.

What’s interesting about the data for the recent household savings rate jumping to @ 10% is that it has been largely funded by a corresponding increase in additional new mortgage (debt) of a similar amount during the same period. This is a transfer of money (credit) from one subsection of society at the household level to another subsection of society at the household level as a deposit. The net effect is the new credit ‘money’ is not being spent back into the economy. If new credit continues to be created by one household group and saved by another household group, it is the functional equivalent of withdrawing the newly created money from economic circulation and will result in marginal borrowers slowly being deprived of the economic access to sufficient money to pay their debts.

I can’t see how it’s possible from an accounting identities perspective, that consumer confidence and retail sales will rebound unless the present conditions change in one or more of the following ways 1. The household sector stops saving (dis-saves) 2. The Govenment increases its deficit (dis-saves) 3. The external sector increases (via balance of trade) the external deficit (external dis-saving).

I cant see how retail can really come back in the foreseeable future without another big round of stimulus anyway. The government 2012/13 surplus going to be looking like a real pipe dream shortly.

China is not deflating

Well what a surprise. After the gov pops a dead market up with a stimulus and takes it away, the market has died again. Leaving more people in high debt. Is the gov dumb or people who borrowed in fuel debt economy? I think both!!!!!.

You cannot stick money on a dead horse and expect it to win. You have to get a new horse invest in it and then stick your money on. Wow I thought we were a smart country.

Is it ozzy ozzy ozzy! ooh! ooh! ooh! or dumb, dumb and duma.!!!!

In truth retail spending and high mortgages cannot exist next to each other. One has to go. Mortgages “Mort” death and Gage to be engaged to. Is exactly what is happening to many families.

If the gov had any duty of care. They would not let this happen. But this gov governs for themselves and not the people. Houses are way over priced and the cost of living well that to.

There is no quick fix just a realisation that we are in deep water and life is not worth living with a massive debt burden so you can tell others you are doing well. Blah. You are rich because you are not because you have.

Thats funny Average Bloke……..

umm China just isnt growing as quickly as before. Seeing that just about everything is made in China now and they still require copius amounts of our energy and mineral resources – how is that funny?

Or do you just find reality, ironic?

This is reality…. looks like they are deflating…….

“But there have been growing concerns among analysts that authorities may have gone too far in trying to slow the world’s second-largest economy and the tightening measures could trigger a hard landing.”

http://www.theaustralian.com.au/business/industry-sectors/beijing-blocks-credit-flood-into-china-economy-to-tame-inflation/story-e6frg96f-1226074314664

They will still have positive growth just not the double digit growth of the last few years.

@ AverageBloke China is looking at ramping up its trade with other nations to buy mineral resources from, this is due to OZ prices get’n to high. At the same time they plan to buy up lots more of our farms to help feed there growing requirements of the mid class in China. Guess what that means for Australia?…… Crash! So forget about China saving us we are toast and so are our house prices and employment prospects, the Government know this is heading our way soon why else do you think that are trying to get a carbon tax up and running? because they are not going to have the same tax take from mineral exports and they still need to pay down the huge debt they have created. Please try to look at the real world not just the headlines in the morning news!