The latest update to the RP Data-Rismark Hedonic Home Value Index, released today, show Australian house prices have now been falling for six consecutive months. House prices in June fell 0.2 percent seasonally adjusted. Capital City home prices have now fallen 2.0 percent for the year to June.

On Tuesday, ratings agency Moody’s warned it was undertaking a re-assessment on the Australian housing and RMBS (Residential Mortgage Backed Securities) markets. It warned that the run up of House prices in Australia over the past decade is only partially explained by fundamentals and that a possibility of a major correction was a material risk for the Australian market. According to Moody’s, the elevated mortgage debt levels in Australia makes the Australian financial system vulnerable, and untested at current levels of indebtedness.

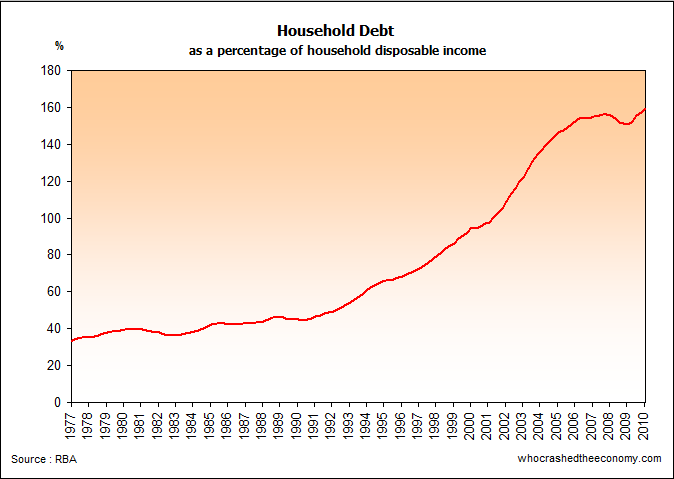

The ABS on Wednesday released figures showing CPI was up 0.9% for the June quarter. This prompted ANZ to tip that Interest Rates could rise as early as next week in a pre-emptive bid to curb spiralling inflation. Any such increase will be a further blow to the housing market, crippled with record levels of household debt.

{kind=link}

Today, ANZ’s Australian Chief, Phil Chronican said the Australian housing market looked “weak” indicating the gains of the past two decades are unlikely to be repeated. He told a business lunch today that he believes the Australia housing market is unaffordable due to unhealthy tax breaks such as negative gearing. ”Governments might want to look at whether the current extent of negative gearing tax breaks are fostering an unhealthy focus on housing as an investment vehicle, thereby compounding affordability issues”. He said housing should be a “a place to live in, sleep, eat and raise your family” and not a speculative investment vehicle.

Earlier in the year, it was made public that the Gillard Government is looking at options of winding back or abolishing Negative Gearing. Negative Gearing requires investors(speculators) to make losses on investments in return for capital gains in the future. Negative gearing doesn’t work all that well in a falling market and our market is expected to continue falling for years to come as we unwind the largest housing bubble in the history of Australia, a bubble exceeding the Melbourne Land Boom that crashed in 1891 and that lead to the Australian Banking Crisis.

» RP Data‐Rismark Hedonic Home Value Index – June rpdata.com, 29th July 2011.

» Australian Capital City House Prices Notch Up Sixth Monthly Fall – The Wall Street Journal, 28th July 2011.

» House prices fall for the sixth straight month – Sydney Morning Herald, 29th July 2011.

» Moody’s warns on Aussie housing market – Macrobusiness, 29th July 2011.

Music to my ears.

When a bank CEO starts complaining about negative gearing you really have to stop and think. I wonder if the banks are getting nervous….

I also wonder if all this ‘negative’ commentary in the main stream media will have any immediate impact (on house prices).

I think another global shock will tip the scales and we are going to see some ugliness.

Don’t you love history !! It has this funny ability of repeating itself.

We are in that space of a housing bust and will be for the next 5 years.

@Free Willy

Yeah maybe the Journalists can’t afford to buy a home either?

JM – you suggest we will be in a bust for the next 5yrs. Look at Japan’s housing bust and how long its lasted! Closer to home in terms of recent memory, look at the US – its continuing down still and likely to go on for some time. A decade of slow decline after a major crash could easily play out, as we’re coming off two decades of overindulgence on cheap credit. You can now buy a whole office building for little more than a pricey house in Sydney in the midwest. Prices are down up to 60% in some of the bubblier states.

It’s about time. When I go house hunting each weekend and look at the prices people are asking the amount of money I would then have to spend fixing it up I just flat out refuse to pay it even if i can afford it. Especially when you look up what they paid for it just a few years ago.

@MissMoneyPenny: I can’t believe someone reading this site is actually house hunting. You’d have to be mad.

@ Juiced:

I am studying the market so when it eventually turns I will be ready. I also like to back up the reported data with my own anecdotal evidence. Watching the real estate agents getting more desperate to sell is a change. Also when I am the only person at the inspection which happens a few times I have a good chat to the agent and find out quite a bit.

One agent told me last week that the places that aren’t selling for 6 months plus with no drop in price is because the vendors refuse to concede that the market has changed. He was telling them that he wouldn’t sell their houses unless they were more realistic. I suppose there is only so long you will show a house every Saturday without making any commission.

I am still waiting for the recession to happen in Sydney. Believe it or not demand is still quite high in some areas and thanks to the banks people are still willing pay ridiculus amounts of money. A 3bdm villa in greater western sydney (Girraween) which is out in the sticks 30km from the centre sold for between $500-$550K. What the? These people have rocks in their head…

The recession may be hitting perth, Queensland and Melbourne especially, but Sydney has a while yet before things start going backwards. Finger crossed!

@MissMoneyPenny

I’m doing what you are doing… its the only way to get some perspective on the market without the hype (main stream media).

Sydney is taking longer to turn the corner that seems to be the case but the prices also seem very up/down (+- $100K on similar places in the same suburb) showing that some vendors are getting desperate.

I was talking to a mortgage broker about loan durations and it surprised me a little when he indicated that they have no problem (these days) providing loans that will extend well into peoples retirement. Then I read the below article.

http://www.couriermail.com.au/ipad/mortgage-pain-to-last-into-retirement/story-fn6ckkri-1225980511053

I think there is going to be a bit of down-sizing / sell to rent going on in the not too distant future (10-20 years).

It makes you wonder what the long term repercussions of these bank policies will be.

Clearly banks are not satisfied with taking 30-40% of your after tax income when you are working, they want most of your retirement/super as well! And this is all driven by lending practices which fuel ballooning property prices (need to mention negative gearing in there somewhere as well)

That Townhouse in Girraween would have been bought by a Negative Geared Property Investor. That’s why they paid the ridiculous price. It’s not that ridiculous when you can charge high rent in a tight rental market and have the taxpayer pay for your losses.

So Gillard is considering abolishing or scaling back negative gearing?

http://www.facebook.com/EndNegativeGearingTaxSubsidy

A mass revolt by young voters on this issue will give her a shove!