A Housing Industry of Australia (HIA) / RP Data residential land report has today shown land sales have fallen to their lowest level since accurate figures were first recorded. In just the past year, Land sales around the country has fallen 43 percent to the end of the March quarter.

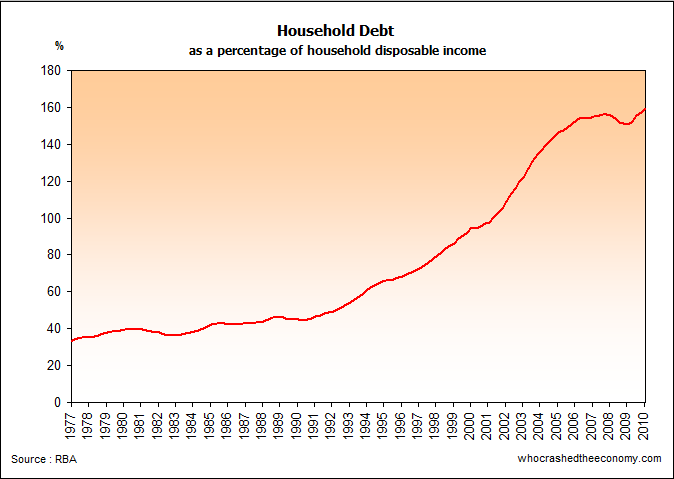

Jonathan Reeves, an economist at the Australian School of Business at the University of NSW has said “It is likely that this is the beginning of a substantial housing correction, because the stimulus effects are continuing to fade”. Australia’s housing bubble, like that many other countries, was built upon a quadrupling of household debt over the past 30 years and started to collapse in 2008 before the Rudd government helped prop it back up with the First Home Buyers Boost. It is increasingly unlikely the Gillard government will do the same time this time around, although with new Global Financial Crises (GFC2s) forming in the Eurozone, further U.S. deterioration from the conclusion of its second big bailout (QE2) and/or its inability to raise the debt ceiling, could cause our government to act again with a knee jerk reaction, further delaying the housing collapse for another year or two depending on the size of the stimulus.

{kind=link}

But it is not only the Australia housing market in Dire Straits. Following an article we wrote in March 2009, titled Housing or Jobs?, we indicated if too much money was directed into housing, discretionary spending would have to fall. This is starting to play out now in shops around the country. Today, department store retailer David Jones, announced trading conditions have deteriorated significantly in April to June, and downgraded profit forecasts. This saw David Jones shares fall 18.16 percent and caused shock waves through the listed retail sector. CEO Paul Zahra, said “The dramatic and rapid deterioration in trading conditions in 4Q11 has been unprecedented,” (We did warn in early April, that there is a lot more pain ahead in terms of retail spending after Net Savings ratios sprung back to levels not seen in 25 years.)

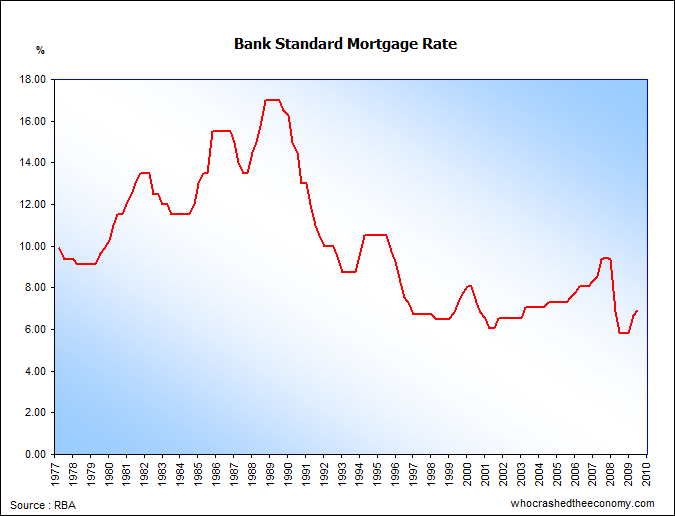

Sadly, mainstream media has yet to pick up on the real cause of the downfall of consumer spending, even going as far to highlight Paul Zahra’s claims that the carbon tax was in part to play. We suspect in subsequent years, the Carbon Tax will be made the scape goat for the 30 so years of irrational debt accumulation. Mainstream media is also lashing out at the RBA for successive interest rate rises, yet the Bank Standard Mortgage Rate is at some of the lowest levels in decades. I can’t recall one instance where the RBA asked Australian households to leverage up in debt. Excessive debt is the real problem, not interest rates.

{kind=link}

Last month we reported on an article from the Unconventional Economist showing that falls in house prices actually cause (or leads) unemployment. It’s often an argument, that house prices can’t fall, because we have record low unemployment hovering around 4.9%. Based on this, and the continue decline in retailing, a sector which is Australia’s largest employer, we expect to see unemployment starting to trend up later in the year.

» DJs blames Gillard government taxes for profit plunge – Thursday July 14 2011.

» Land sales at lowest level in 10 years – Thursday 14th July 2011.

» RESIDENTIAL land sales have slid to their lowest level in 10 years, according to a report. – The Australian, 14th July 2011.

May I say that this hasn’t come out of the blue? That for quite a number of years now those of us that opened at least one eye in the land of the blind kept saying, its’ coming, its’ coming. Its’ come, is so unexpected?

I won’t speak about what many of us already know regarding the mainstream media, the non-fictional unemployment rate, true inflation rate, and also the highly esteemed Bloggist, Unconventional Economist and the rest of the top crew at MacroBusiness.

Big underclass will develop in Australia. Will be the way things will be from here on, or for a long time to come.

Guess my luck came when I was young and my parents taught me to save, spend only what I could expend, and cut up the Credit Card, back then it was called a Bank Card. I say this cause I portion much of this cause coming from the debt stricten.

Its’ not the interest rate that kills. Its’ the principal. If many weren’t carrying so much debt, all these price rises occurring (energy, food, medical care) would be a bummer NOT a show stopper.

Hmm yes this maybe the start. But I suspect that the Government will use stimulus in the very near future and kick start the ponzi bubble yet again.

The 2nd link is quite a laugh – It has a quote from HIA’s chief economist Harley Dale saying “Softer demand is part of the story and the dizzy heights sometimes reached in speculation regarding a fictitious housing bubble in Australia certainly doesn’t do anything for home building confidence,”

Fictitious housing bubble? Sounds a bit like Ben Bernanke who said in October 2005 the U.S. had no bubble, hence it also couldn’t pop.

G’Day AverageBloke, that will take tonnes of money that will need to come from somewhere. I say such a silly thing cause our gracious Government of Benevolence and Compassion doesn’t have it. So a revenue stream will come from a form of new or existing taxation. As tax revenue is down and on the way further down, our Governement (the Benevolent and Compassionate) will borrow lots more of it on top of the tonnes it has already, leading us to a situation nobody will want to be in. The Average-Bloke out there is already screaming in pain over large increases in day-to-day living expenses. Hope this isn’t funding this ponzi bubble.

In case we’re not drunk enough, my friend earns a little more than $66K p.a, little savings and well into his 40s was offered a home loan for $700K. Has been renting for years and does not own a property. If things like this are keeping the ponzi afloat, oh boy! No wonder we’re strong leader (I think we usurped the North Americans from pole position) in personal debt. And we may start aggressively competing in Government debt too. I’m looking at Greece and here and no longer think, ha! we won’t go down that raod cause of all the holes in the ground. Now I thinking, just how much debt can we drown in because of all the holes in the ground.

By the way, I meant to ask you, how long do you reckon this Ponzi can go on for?

@Average Bloke.

I don’t think the Govt will kick start the bubble as it has already hit the peak and families are maxed out on credit and struggling with living costs. I think people aren’t that foolish, although I could be wrong.

This is just the beginning of the retail decline, whom are Australias biggest employer and account for 11% of GDP.

Should this trend continue, it is Inevitable that unemployment will rise and this is the key to a substantial housing correction.

Another stimulus doubt it!! Tax breaks most likely.

Another stimulus would be stupidity. Will the government go to court for there “ill or lack of duty of care”. Prying on the poor and missinformed.??????????

I am patiently waiting, renting and saving. While I feel sympathy for the people that didn’t see this coming I hope it corrects soon for all of the responsible savers in Australia that didn’t overload themselves with debt. If there is further stimulus it will just delay the inevitable and won’t help anyone (except retailers in the short-term).

Good article but i have a different interpretation. I am a real estate agent and have been for 18 years. I know you will label me the property spruiker bullshit. However I will tell you what will happen. Retail is exceptionally tough all over the country and with the online buying trend, retail is in a new world. It is too bigger part of the economy to not support. This support will come in the form of interest rate reductions. Interest rates have already peaked andi have been saying it for 6 months. Property markets love interest rate stability and certainly cuts. I don’t expect it to boom but it will firm. Unemployment will rise, simply because that is the next part of the cycle. But it will not rise dramatically. I know it does not make sensational headlines but Australia is in for a steady ride. Enjoy it, these years they are the golden years and thanks to china, we have a few to come. Ok let it rip, bubble boys and doomsayers, I’m looking forward to the debate.

Nt

Marty Farty had a party, all his mates were there, Judy Cutie did a beauty they all went out for air.

There you go Marty, I let one rip for you.

Hi everyone,

I agree with what everyone is saying here but you must remember the Government can be influenced quite easily by the RE industry and other vested interests to make irrational short -term decisions – look at the last few years as an example.

Add to that we have one of the lowest govt debt to gdp ratios in the western world and I can smell the possiblilty of a further stimulus.

Personally I hope not but as we’ve recently seen here in Queensland the RE and Building only have to make a whimper and the State Government will raid it’s dwindling coffers for housing stimulus.

This is lively debate, so feel free to put your point of view across in regards to my thoughts and comments.

@Marty

Your comments are noted, but these so called Golden years have only benefited large companies & shareholders. Any benefit or surplus the government gets goes towards failed insulation schemes, govt hand outs or proping up the housing bubble. The average family on average wages (not mining wages) is worse off than they’ve ever been with a huge portion of their NETT income gobbled up in DEPT & mortgage repayments. The big issue is not so much interest rates, but DEPT..DEPT..DEPT.

Reducing interest rates will have little impact this time around as prices are much higher (up to 30% in some areas of Sydney) now than they were post GFC when Labor introduced the 1st home owners boost. People aren’t that gullible any more and banks are putting a squeeze on their lending.

The tax system in Australia, i.e Negative gearing allows highly leveraged investors to speculate on property, which deteriorates affordability and creates bubbles – no doubt about it. With the housing market heading south, many investor are selling up fast and this makes NG redundant.

There were some Australian Treasury Executive Minutes released about the FHOB saying “The short term stimulus was designed to encourage people who had already been saving for a home to bring forward their purchase and prevent the collapse of the housing market.”

With some of these Treasury Minutes now in the public domain, the public is getting a clearer perception on what really went on during those weeks and months following the collapse of Lehman Brothers. Treasury knew there was a housing bubble, and clearly they encouraged the first home owner already saving for a home to bring forward their purchases and prevent the collapse of the Australian housing market in 2008.

The problem now at hand is the political fallout when those first home owners start defaulting on their homes (10 percent have already sold) and the mainstream works out what happened. How many First Home Buyers jumped on the bandwagon during the period of the boost?

Will the fallout mean the government has to bail out those first home buyers who purchased homes under false pretences of the government in 2008, or will the Australian public be a little more educated this time around on what the real intention is? Will new first home owners jump on the new stimulus bandwagon when it sees what happen to the last cohort?

@ Tom,

You are assuming that the general public would find the information about the Treasury minutes. I remember reading them months ago and thinking how could people buy a house now if that is what the Treasury is saying. If it is not in the main stream media most people won’t bother finding it (which doesn’t mean they should not research more thoroughly the large purchase of a house).

@MissMoneyPenny, yes, you are right although I believe it was published by one of the papers a couple of months ago. However, I would suspect if Labour was to introduce another housing stimulus, Liberals would be out there to prove Labour’s bad economic management. This could be just the thing to prove that Labour knew what they were doing when they introduced the boost.

that poor old bubble. it must be getting very tired by now, hardly able to stay afloat with all the props underneath it. one of those props could pop it………any time now.

there are a number of forecasts of a really big global financial crisis towards the end of this year, the 2008 event being merely a slight hickup. bubbles everywhere could become an endangered species.

http://www.leap2020.eu/GEAB-N-56-Special-Summer-2011-is-available-Global-systemic-crisis-Last-warning-before-the-Autumn-2011-shock-when-15_a6679.html

Thanks Judy, very artistic of you. Dominic, I accept what you re saying.

We need to accept that the Australian property market is not just one property market, but many smaller markets affected by different local drivers with the main overarching common denominator being sentiment. There are always three factors that drive property markets: supply, demand and sentiment.

If you look at the last 12 months, Queensland had record rains which severely affected that market, not just through floods but through their impact on tourism which is the lifeblood of much of their coastal economy. Yet in Perth they were in drought and their property market has completely different drivers. Their property market overcooked in the last cycle due to over positive sentiment of the mining boom. It has been soft for a few years but look what is about to happen again, many pundits are talking up Perth again because of the massive mining investment

Sorry pressed the submit button accidentally! Anyway the point I’m am making is that sentiment is very important to property markets, just like it is the share market. Interest rates reversing in trend provides an overarching positive sentiment that will have different levels of impact depending on the local drivers in your location. But most would agree that a reducing interest rate trend is likely to provide an overall positive sentiment to their situation.

This is why I believe the property market in a general sense will stay firm. Especially since it has held quite well in the face of such a determined Australian media campaign to talk it down. No one is suggesting that there is an over supply of property and last time I looked we are still at full employment.

“…and last time I looked we are still at full employment.”

Yes Marty, the last time employees from CentreLink, MissionAustralia, and The Salvation Army looked (as MA and SA are “Employment Service Providers” for CentreLink). The number of people registering with them (MA and SA) to attain a benefit is not indicative of an economy with 4.9% unemployment, not even indicative of an economy with 7.5% unemployment. Welfare is a booming industry.

Remember before CentreLink was called CentreLink it was called the DSS (Department of Social Security), and before that it was called the CES (Commonwealth Employment Service)? When it was called the CES, you could apply (not necessarily attain, but apply) for some kind of bebefit or assistance if your working hours were 14 hours per week or less. Now its’ 1 hour a week. Why? (Rhetorical). If the last time you looked was 8 years ago then fair comment. But you didn’t look yesterday.

Interest rates, I can’t make a call on that as interest rates around the rest of the world are near zero. All that has seemed to cause is civil unrest, and no solutions. Its’ not interest rates that kill, its’ the amount borrowed and speaking of which, Australians are quickly becoming champions of personal debt. Big problem. As you can see, you’re really not running a store selling hot cakes, and what you’re selling you seem to have a lot of it. That’s indicative of what is on display for all to see.

“For Sale”

“No one is suggesting that there is an over supply of property…..”

You must be living somewhere outside of Australia! There is an abundant over supply of houses in Aus. I can’t believe someone who professes to be in the industry can make such a blind comment. The rises in houses for sale now compared to six months ago proves this! That’s one such indicator. Then there are the no. persons per house ratio, it’s been dropping for years, then theres the fact there are 800,000 vacant homes in Australia…etc. etc.

Comments such as that deserve to be treated the same way as “now’s the time to buy, or be locked out”. Utter trash, and will be proved to be such in time.

The media hasn’t been talking the market down that much Marty. Why would they kick their cash cow? That kick it a little just so the average blokes out there can have a little sliver of hope of home ownership.

No actually I agree with you Marty that the housing market will stay stable thanks to Neagtively Geared Investors and a tight rental market.

AverageBloke, the reantal market will loosen up. There are tonnes of units and houses that have just entered the rental market. That’s just now.

I agree with you on Negative Gearing staying for the long haul, but will it save the day in the long run? Westpac Bank doesn’t look like it wants to continue its’ Benevolence of Credit scheme. I don’t think a reduction in interest rates will help out many people with their huge debt obligations. People are screaming over their utility bills, food, and petrol just to name a few. I think another or first mortagage hasn’t come on the horizon for them yet.

How many (even poptential) property investors are there, enough to keep the ponzi going?

Future will tell.

Marty, you would be a member of the REIV?

Are you able to comment on this :

http://www.theage.com.au/victoria/auction-statistics-questioned-20110716-1hj4h.html

They are suggesting Auction Clearance rates are actually under 33% in your State

1. Unemployment will jump “more than expected” due to retail and building industry crash

The key to a property market correction is unemployment because most people cannot borrow or pay mortgages without an income.

Retail trade employs more people than any other industry in any state in Australia (even WA where it accounts for approx 14%). The decline (in retail) is already in progress watch this space…..

When you add the building industry (with building starts falling off a cliff) you have the perfect storm.

2. Property inventory levels will explode

This will occur as investors which make up about 50% of the population try to exit the market. Inventory levels are already going through the roof (as an indication of this).

The fallacy of under-supply (of property) has now been proven (by increasing inventory levels). The abode to person ratio has already proven that there are way more homes in Australia than people.

The trigger for the exit (by investors) will be unemployment and stagnating or declining asset (house) prices and the urge for profit taking (creating a positive feedback loop). Anyone who has “invested” or purchased in the last 3-5 years will likely be in this category

3. Contributing factors to housing collapse

When times get tough, people get creative. Young couples and singles will move back home with their folks. If they are renting then they will exist the rental market; if they are in debt they may declare bankruptcy and walk away. This will create move available property (rent/buy)

4. Rental Income will Drop

Due to 3 and also 2. As inventory levels increase some owners that can’t get the price they want for their investment at sale/auction will attempt to rent it out (this is already happening) causing a flood of rental properties which will drive rental returns down even further

5. Interest rates won’t drop much

The RBA doesn’t control them, more than 50% of the funding for our property market sourced offshore and they (the foreigners) want the risk premium factored into the interest on the debt. Did you notice how our banks didn’t pass on all the discounts and increase rates higher than the RBA (down/up)

And so there will be no “magic bullet” from the RBA. The increase in cost of living that has happened in the past 2 years (increases in power, food, petrol costs) is eroding any drop in interest rates anyway.

For interest rates to really drop, all the external debt ($600 billion+) would need to be taken up by the RBA (e.g. printing money).

6. Flood of new buyers

The idea that will drastically lowering house prices there will be a flood of buyers to take up the slack is another fallacy. Too many Aussies have too much debt to do this. The number of cashed up couples is far lower than that of the debt laden donkeys.

Money will be scarce because the banks will be in trouble; very risk averse and selective as to whom they are going to give the $$$ they can give out (think 20%+ deposit).

7. GFC2 – By end of year

The US and Europe are not recovering. GFC2 will make global money very tight; relates to #5 above and will impact any remaining buyers that need to borrow.

Ok boys, here goes, in order of reply:

Botrot: most economists regard anything under 5% unemployment as “full employment”. Doesnt make sense to me either but that is what they generally label it. I’ve got an idea: why don’t we express the stat as 95% employment. It would make us all feel a lot better. It won’t happen because the glass half empty dude that designed this website would run around telling everyone that life wasn’t meant to be this good.

Matty, so there,s 800,000 vacant homes is there? Why are we so worried about 2000 boat people coming to Australia? We have heaps of homes for them. I would also suggest that most homes for sale would actually have someone living in them. The amount of homes that are for sale has certainly built up. It’s called supply. When supply builds up because there not being sold, the property market flattens. OMG look what’s happened, the supply has built up and the market has flattened! Asset markets are cyclical, property markets are no different. I started selling homes in 1993, I seen the market peak and flatten through 3 cycles in that time. This cycle is no different.

Averagebloke: we are probably seeing from different sides. There consistent negative language just annoys me. They have this mission to pump as much misery into our lives as possible. They actually do have have a reason to talk it down, they are trying to extend the days on market so a vendor has to advertise longer to sell. I stopped using print media because I just couldn’t justify the expense to my vendors.

Tom: this is a definition thing. Chris vedelago has alway hated agents. He has been riding this issue for a while now. What the REIV is saying is that if an advertised auction campaign has caused the property to sell, whether it is prior to the auction, under the hammer or after the auction on that day it can be regarded as being sold at auction because the parties were drawn to that property, on that day by the scheduled auction. I think the definition is reasonable, if you don’t agree, and Chris V doesn’t because he hates agents, you can try and get a negative headline from it.

Free Willy: mate, your glass is so empty I can’t help you. The world is not such a terrible place. Peace brother.

I’ve enjoyed the chat boys, take care. MM

“…why don

Marty I check the MSM newspaper property sections nearly everyday and the Negative Vs Positive RE articles are about 50-50 in my opinion. To be fair mate during, the Skyrocketing House Price Orgy of the last 10 yrs the MSM has Spruiked the crap out of the market it’s only now that I’m seeing some negative articles.

Why are RE agents complaining? Is it because they actually have to do some work now?

As you have picked up there are many like myself who view the RE market at the polar opposite to RE agents. Whenever I see an Investor Spruik article I get very depressed as I see my future of owning a modest home to have financial security for myself and my family be taken away. Whenever I see a rational article about how the market is flattening out or even dropping a bit I see a bit hope that my savings haven’t been in vain.

@ Marty what’s up mate did I scare you away with a few facts and god forbid – evidence. I know, reality is over-rated.

As a not so famous movie once told me, if you’re gonna be a bear, BE A GRIZZLY! LOL

Sorry guys I have been away for a week on holidays, so wasn’t scared off Free Willy.

Average guy, I accept that the numbers to get into the market are now significantly more than what they were. I genuinely do not believe property spruikers, as you like to call them, make that much different to the overall market. Like you many people aspire to own a property and that’s what drives the market more than anything. When they decide to do it all at the same time that’s when property markets firm. It is the great Australian dream, a dream that is not as strong anywhere else in the world ( it appears) Saying the world is about to crash doesn’t change anything except get you more depressed, unnecessarily in my opinion. I just get annoyed that the mainstream media has the right to pump as much misery into our lives and often these forums just want depress and scare people as much as possible. Sorry for saying hey I think we are going to be ok.

Free willy, let’s touch base in 6 months and see what happens. My version is that interest rates have peaked and the next move is down. This will significantly help sentiment. Craig James, who I think is the most level headed economist is forecasting the stock market will get to 5000 points by the end of the year. If it does sentiment will improve. It is very rare that the property market does not follow the stock market in terms of trends. No one is predicting that their is a boom ahead but just don’t expect a free fall. No matter how much you grizzle.

Glendora, it always comes down to three simple rules, supply, demand and sentiment. As I said earlier each individual area in Australia often have different drivers and are affected by both local and national factors. Many suburbs in the capital cities have performed very well in this softer market due to the specific factors of that market place. I haven’t got a clue about Parramatta, but if people want to live there and supply is limited, prices will rise or at least hold. It’s pretty simple.

@ Marty

The stock market is a leading indicator for all other markets and in your words “It is very rare that the property market does not follow the stock market in terms of trends”. Looks like my call was a little late…. this weeks market results are awe inspiring and this is just the beginning! Add retail figures posted in the last week to this – worst retail growth in 50 years!

http://www.news.com.au/money/shopping-strike-worst-in-50-years/story-e6frfmci-1226107951792

What do you think saved the ASX200 after the GFC….. STIMULUS! the ‘wealth effect’ [for Keynesian’s] but what goes up (artificially) must come down (very hard). Look at the Dow and Nasdaq and correlate them with QE1 and QE2 and then look at US employment and Retail growth data…. bit of a pattern emerging there.

A couple of years back interest rates were at their lowest levels in 50 years. They haven’t gone up much at all (still at an average low) and people are screaming that they are too high…. why is that? Simply because of the amount of leverage they have. I will concede that interest rates probably will go down in a desperate attempt for regulators to intervene in the natural market flows once again! (so much for efficient market theory!) but this won’t save the goose because our employment figures are a farce.

You have to understand the US economy has been on life support (quantitative easing) for 3 years. And last month they pulled the plug. We are now seeing the results and boy is it going to get interesting… add Europe to the mix and we are in for one hell of a show. China is linked to US/Europe and we are chained to China.

This is not doom-saying, in fact I think it would be a wonderful place if mum OR dad could have a choice to go to work and still own a home and if i’m right and there is an implosion, the next generation will be able to do just this! The cost will be to the current generation. Western civilisation is the most time poor on the planet… why is that?