There is growing concerns Australia’s miracle economy might not be in as good shape as our politicians would lead us to believe. This view was reinforced today when the Reserve Bank of Australia was forced to cut official interest rates to help stave off what could emerge as the second stage of the GFC. Treasurer Wayne Swan said today, “these cuts have been made responsible by our responsible budget policy. Today, at 3.25 per cent, the official cash rate is lower than it was at any time under the last Liberal government.”

The central bank slashed another 25 basis points from the cash rate today, adjusting the leaver down one notch to 3.25 per cent. It is just 25 basis points off the low recorded during the Global Financial Crisis (stage I).

The statement on today’s monetary policy decision shows the central bank is concerned about the outlook of the world economy, especially growth in China. It notes commodity prices remain significantly lower.

Back home, it notes “investment in dwellings has remained subdued” and makes an assessment that the labour market has “softened somewhat” in recent months.

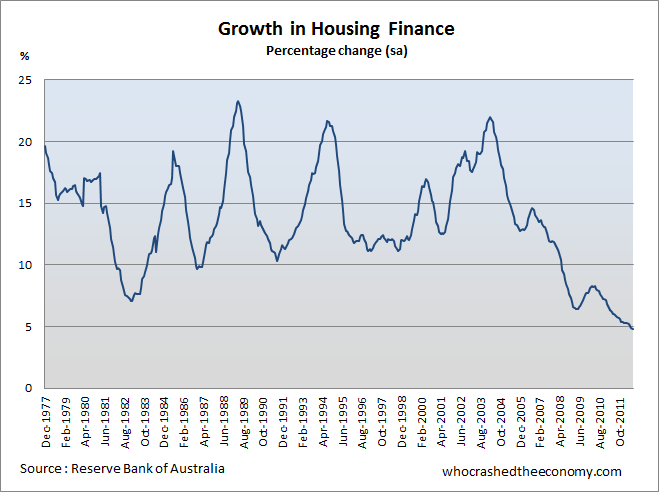

Last Friday the RBA released its August update of its financial aggregates painting another bleak picture for housing. Growth in housing finance continues to fall and sits at “subdued” levels not seen since records started 35 years ago. Hardly the foundation required for a recovery.

Last week, reports surfaced showing new home building is at levels not seen in 15 years.

Analysis by Leith van Onselen @ Macrobusiness shows a “softened” labour market. In non-seasonally adjusted terms, the labour market contracted at record levels (dating back to 1985) in the August quarter, losing 135,500 positions. No prizes for guessing construction lead the job losses in raw number terms, followed by agriculture and public service positions.

While mortgage rates may be approaching record lows, aggregate data shows households are still paying more in interest payments as a percentage of household disposable income, than in 1989 when rates approached the 17 per cent mark. How is that, you ask?

While households are making some inroads into deleveraging their balance sheets, it is very hard to see any recovery while household debt levels remain excessively elevated and the risks of broad based job losses increase.

» Global economy prompts Australian interest rate cut – The 7:30 report (ABC), 2nd October 2012.

» Australia’s record quarterly job losses – Macrobusiness, 18th September 2012.

The wheels are starting to fall off. How many weeks before a housing stimulus package is announced?

There is so much focus on making money out of housing and mining in this country while any innovation or research and development has gone. If iron ore and coal keep falling then what do we have left? Answer: Expensive houses and lots of big holes around the country. If it seems to good to be true then it probably is.

OK, so they cut rates in line with the expected “Low rates good, high rates bad” mantra to placate the ignorant masses, thus igniting a new surge of appetite for residential housing investment debt.

Where are the macro-prudential measures to give effect to Captn Glenn’s “Glass half full” speech:

Remember this:

One thing we should not do, in my judgement, is try to engineer a return to the boom. Many people say that we need more ‘confidence’ in the economy among both households and businesses. We do, but it has to be the right sort of confidence. The kind of confidence based on nothing more than expectations of ever-increasing housing prices, with the associated willingness to continue increasing leverage, on the assumption that this is a sure way to wealth, would not be the right kind. Unfortunately, we have been rather too prone to that misplaced optimism on occasion. You don’t have to be a believer in bubbles to think that a return to sizeable price increases and higher household gearing from still reasonably high current levels would be a risky approach. It would surely be a false basis for confidence. The intended effect of recent policy actions is certainly not to pump up speculative demand for assets.[6] As it happens, our judgement is that the risk of reigniting a boom in borrowing and prices is not very high, and this was a key consideration in decisions to lower interest rates over the past eight months.

http://www.rba.gov.au/speeches/2012/sp-gov-080612.html

So Captn, over to you. How are you going to stop the fools rushing in? Pro tip: Pick up the phone to your compatriate in Canada.

Yesterdays rate cut is a sure sign that the central government goons are realizing that the economy is now at the beginning of a death dive. The years of money printing by the large economies have created a massive currency war,in which the RBA has now entered in to compete with US,EEC,Japan etc money printing which has devalued their currencies.The RBA has now thrown the rule book out in terms of its charter of fighting inflation and knows full well that inflation is running higher than its published CPI figure.Only a fool would ignore the cost of living has rocketed over the last 3 years especially on everyday normal living costs ie Electricity, gas,insurance,car rego,water and council rates.The RBA will try to inflate the economy again like 2008 creating a false boom,the lowering of rates is a call to people to borrow more and more in a effort to reinflate asset prices and further more the aussie dollar is not going to fall like it did during the GFC because of the perpetual money printing overseas which is resulting in the destruction of our secondary industries.Another downside is the RBA is wanting to keep house prices high and has stated that investment in housing is at near all time lows.Basically residential investment is a non productive investment in which many people have sought to increase their wealth and returns are at all time lows especially in Melbourne and S.E. QLD.The RBA wants to continue funnelling money into housing where there is a glut.Unfortunately the RBA is a mouthpiece for the international financiers sending us down the road to what is happening in USA and Europe which is the destruction of industry,the buying power of your money destroyed,increase in debt levels both private and public.Until such time interest rates are set by the market to reflect risk the death dive will continue unabated.

Top article on Spain et al.

http://finance.fortune.cnn.com/2012/10/02/spain-fear-the-worst/?iid=HP_LN

The Question must be asked, What makes us immune?

Young relatives recently put down a deposit on a shitty $170,000, 600 m2 block of land.

God almighty I’m thinking.

This is just indentured slavery of our young people.

Casualisation of our workforce, destruction of our manufacturing industries and the financial export (ownership) of the inherent wealth tied up in our farming and primary production industries.

Yet we pump more air into the housing bubble, so that Mr Swan can climb on top of it, look around and tell us everything is ok.

Sure, everything is ok, if you believe it’s perfectly natural to be so indebted to the point that it consumes your entire life!

And the full-force of the European debt tsunami is yet to crash over the Chinese sea-wall and inundate the mortgage flood-plains of debt-ridden middle and lower class Australia.

Mass misery coming to a suburb near you.