In an interview with Neil Mitchell’s 3AW on Friday, Prime Minister Abbott said “Don’t forget Neil that if housing prices go up, sure that makes it harder to get into the market, but it also means that everyone who is in the market has a more valuable asset.”

His comment prompted Neil Mitchell to respond prudently with, “But interest rates can’t stay at this level, people are going to get burnt!”

Abbott shunned any responsibility, lumping it on the central bank by saying, “I am sure the Reserve Bank is very conscious of the fact that there are a whole range of things that need to be managed here and I would be confident that the Reserve has got its eye on housing prices and will appropriately manage the level of interest rates.”

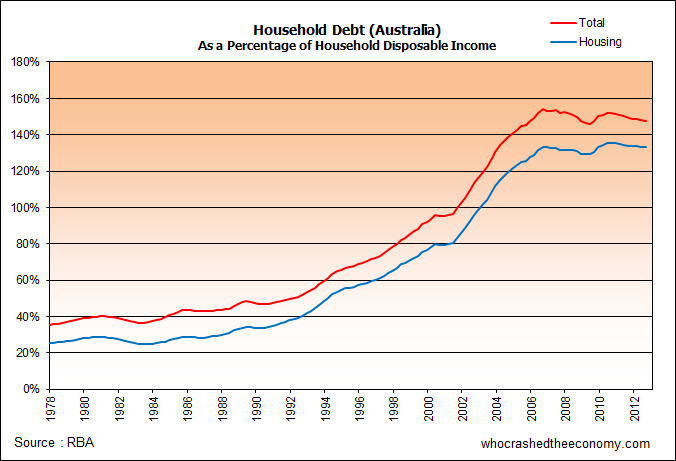

His ignorance is likely to have heads shaking at the Reserve Bank of Australia (RBA), Australian Prudential Regulation Authority (APRA) and even the International Monetary Fund (IMF) who have all been sounding alarm bells in recent weeks.

Australia’s housing bubble and associated household debt is acting as a leech, sucking blood out of the economy. In the low interest rate environment, The RBA is struggling to keep the housing market under control, while supporting the faltering broader economy and attempting to cool the strong Australian dollar.

{kind=link}

One of the causes of euphoria in the housing market is a broken taxation system, severely distorting the economy and something clearly the responsibility of the Federal Government, not the Reserve Bank. Two Howard Era tax concessions instantly spring to mind.

The 50% capital gains discount introduced in 1999 – when coupled with negative gearing introduced decades earlier, accelerated the accumulated loses of residential property investor making the playground much more geared towards speculative capital gains and not rental yield.

{kind=link}

And the hot topic in the recent months – Allowing Self Managed Super Funds (SMSFs) the ability to borrow and leverage up into the property bubble, introduced by Liberal’s in September 2007. This not only creates a risk for the residential property market, but has severe implications for our superannuation system as well.

Abbott is hoping renewed confidence in the housing market will result in more homes being built – alleviating some of the supply side constraints. However, this could be flawed thinking as there is little evidence to date to suggest this will happen as most speculators play in the established residential housing market. If Abbott wanted to show some leadership and create a tangible outcome, he could quarantine negative gearing and make it only available for new dwellings.

Australia’s housing bubble is a significant issue that needs the concerted effort of the Federal Government, the RBA and APRA. Setting the Reserve Bank up to fail shows both poor leadership and poor form.

» Interview with Neil Mitchell, Radio 3AW, Melbourne – The Prime Minister of Australia, 27th September 2013.

Saying what should happen and what will happen are two completely different things. Tony Abbott, like all other politicians are committed to high housing prices, so we can safely assume that he will not do anything to pop the bubble. Nor will any other politician, as we have seen with Rudd/Gillard and with John Howard.

The bubble is now too big to pop intentionally, knowing it will cause untold damage. The easiest thing to do, therefore is to ignore the problem. I am sure Abbott is hoping the bubble continues to grow under his leadership, and if it pops some time later, well, he can’t be blamed.

Nobody, but NOBODY will take any responsible leadership type of action for fear of offending the vested interests. The only solution is to wait, and hope and pray that they don’t take any active measures to inflate the bubble even more, but of course I think that’s a hopeless cause. Eventually it will run out of steam, but who can say when?

Meanwhile, pumping the bubble harder will prolong the agony and at the same time, everybody’s lifestyle is worse off because of the policies supporting it. We have to put up with more traffic congestion because of the high immigration rate needed to keep this Ponzi going. We have to have a large group of people shut out of home-ownership in favour of subsidised investors and worse, foreign investors, bidding up prices. And anyone who does take on the burden of a high mortgage has to subject themselves to the stress of huge debt for many years, along with all the repercussions there.

In hindsight, there will be many books and articles written about how we were complicit in the biggest Ponzi scheme ever, and the aftermath of it. But in the meantime, we’re stuck in this ridiculous situation, and just have to hope that the politicians of the day will choose the less stupid options rather than the most stupid.

I cannot believe my ears and eyes. This person is the PM of this country? I am fast losing respect for the conscientious voter. One more reason to see who most politicians truly are. Born into privilege, money and wealth, they have no idea or clue as to what is to struggle on an average salary that is fast losing ground to ever increasing costs of living and then to worry all your life on whether you will keep or lose your job. Most Politicians are obviously dangerous to financial stability and the bottom line is only building and maintaining their voter base and nothing else and the majority of voters are to blame. For decades the political scene in Australia has been ruled by only two political entities. No third or even fourth political party option has ever been given a chance to govern. No thorough political scrutiny is given to politicians personal backgrounds, their supporters, financial backers etc. etc. etc. I believe we will all soon pay the price for our political immaturity.

When the bubble bursts who will be blamed for the carnage that unfolds?

My bet those who lived within their means, banked their savings and refused to borrow and spend will get the blame. Those evil savers who crashed the economy by hoarding cash instead of using it to lever into property, denying the speculators the funds needed to consume, borrow and spend.

These evil savers will be targeted by government and have their savings taxed into oblivion or confiscated to bail out the speculators. They will be demonised by the media and set upon by the tax office.

It’s funny how so soon after the election that bubble trouble talk has arisen.

It is a chance to pass the problem Lock Stock onto the new govt and they will be judged accordingly as to their response.

It’s like a hot potato and is probably a running joke in Canberra to see who gets caught holding the can!

Increased spending coming from anywhere – including debt – results in ‘positive looking’ numbers on spending, consumption and GDP. Hence making the politicians of the day appear to be economic leaders of unparalleled quality.

The housing sector is just another one that feeds into it. Inflate paper value and it makes people feel richer, the country feels richer and more is spent further improving the numbers. To the detriment of the nation, whether it is good for the country or not almost becomes irrelevant.

It’s understandable why politicians on both sides of the fence want this to continue, no one wants to be looking for a chair when the music stops.

The economy moves in cycles, it always has and always will. We all know another one is around the corner, we just don’t know when, or how big the next crash will be.

As with all things, time will tell.

On a side note, I was shocked when they took the decision to allow superannuation accounts to purchase property. I suppose there aren’t too many other areas that can help prop it up.

How amazed and stunned I feel from the few people I know well, who have that; big house with a bigger mortgage, 2 very pricey (but not exclusive) cars, kids in high heeled private schools, more than one of each electronic gadget in their household, etc. Either no money at months end, or the household is subsidised with credit cards. 7 of them in one case. Despite having mountains on their minds, with a facial expression that shows it, they believe (to themselves) that they are rich. While a $30 outing to a coffee shop requires discussion and planning.

They go beyond feeling rich, they not only believe they have more in common with the Rothschilds, Rockefellas of this world, than they do with someone on 48K/pa living in Sydney’s outer-suburbs (which they have more in common with), they also subscribe to policies/regulations that benefit those that are ripping them off. For example, use the super-fund for a property.

With a huge mortgage, substantial personal loans/debt either by credit card or other means, such people see themselves above everyone else, rather than their real position that is, the bottom of the barrel.

That’s the mentality we’re amongst here. The pollies know it, actually the FIRE sector know it too, and when things go belly up, well, you know who is able to walk away from it all.

In case you believe your fellow person is smart, Doctors, Dentist, Barristers, Pilots, etc, have been conned by Real Estate Agents and Financial Advisors.

Abbott ain’t dumb, whatever happens, he will can walk away, an election loss washes his hands, and he’s alright jack. People are dumb, and insane!

We all know a Stanley BotRot!

https://www.youtube.com/watch?v=r0HX4a5P8eE

Honestly Tony Abbott is quite possibly the most ignorant politician I have seen in many years over a large number of issues he is pretty much a Australian George Bush Jnr.

Mind due he “could” be playing good cop/bad cop. The NZ Prime Minister “appeared” to be against the NZ Reserve bank changes with loan to value ratio’s however suspiciously did nothing to change it.

Its unpopular for a politician to say “hey its actually a good thing if your largest asset drops in paper value”. The mainstream media will always sensationalise and take the opposite view to raise the click count.

Its a hope!

I don’t think the Reserve bank can raise interest rates more than 2% at best and they know it. There is simply too much debt and too many debt holders that are highly geared. I think that if rates went above 7% the entire economy would implode because you would several hundred thousand defaults within 90 days and we would be less 4 banks – tax payer bail out of say $150B (goodbye savings accounts).

When you combine this with the size of our market and the allowed foreign investment, twisted tax policy on property (NG, Self Managed Super Funds = 300B and growing and up to 60-70% can go into property), reduced capital gains etc) prices aren’t going down anytime soon.

Add to this monetary policy where we are chasing the US dollar to the bottom (RBA target is 85c); the RBA would be happy to print money(they have stopped for the moment; after then introduced covered bonds which put our savings at further risk) and devalue our currency. A lower dollar makes Australia more attractive as a foreign investor.

They key is unemployment and whilst it’s been increasing it hasn’t had any real impact on house prices in the past 5 years. Who are the biggest employers in Australia? Building and Retail.

There seems to be a pattern emerging here….

Real money might be safer under your bed. like people were doing 100 years ago. Super would have to be the bigest scam.

#8 Simon. I have been thinking the same thing for the last year! you nailed it; he is the Bush Jr. of Australia. I would feel embarrassed to be Australian and have this tool representing my country. I don’t feel much better with my “leadership”. I am Canadian, wife is Australian. We spent the last few years in suburban Sydney. I wish we could live in Sydney proper ie the Northern Beaches… perhaps freshwater but the fact is prices are ridiculous. We relocated back to Vancouver where prices are ridiculous but at least we can get by. Why do people hope interest rates will go lower???….so their mortgage payments are lower; so they can afford “more house”. This is insanity we are hoping rates are lower (meaning the economy as a whole is suffering) so we can afford a more expensive home. Lower rates mean a shi#tier economy which means you might not have a job at all to pay off your massive mortgage.

It is crazy. We were approved for a $747k mortgage when we were in Sydney. When the bank (ANZ) told us that we laughed and said we would have to live to 200 to pay that off at historical rates. No wonder tear down dumps are going for $1 million + if suckers are taking these mortgages.

Please read greaterfool.ca for some Canadian insight; I believe we are very similar…eh?

Tswd from Vancouver

I enjoy reading Garth Turners blog but have challenged him on his endorsements of REIT’s and everything American, only to be labelled a ‘doomer’ or ‘metal head’.

Either houses are homes to live in, or they are investments. If the latter, then house prices must continue to rise – in which case we will continue to support house purchases with Government guarantees, tax breaks and subsidies, so that demand doesn’t fall through the floor due to people spending ever more of their income on houses. This does make some sort of sense: people need to save for their old age, and since Government has tied itself into a straitjacket that prevents it using public debt for its real purpose – to provide safe savings vehicles for citizens – property is a reasonable substitute. But don’t then provide pensions, health care and social care to the asset-rich elderly from the taxes of the young who are also trying to buy houses at far higher prices than the elderly ever paid. Let the elderly sell their assets and live on the proceeds. After all, that’s what savings are for.

But we don’t have to do this. We can restore housing to its real purpose, which is to be homes for people to live in. We can build or renovate enough properties to ensure that supply matches demand, so that house prices are not constantly driven upwards by supply shortages. We can tax away unearned profits on unimproved land, and we can tax away profits from speculative investment in property. We can allow government debt to become the preferred savings vehicle for ordinary people, issuing as much of it as people want to buy and using the proceeds to upgrade our national infrastructure and support domestic enterprise. And we can stop draining our economy to support a bloated property market.

From Pieria.co.uk

Perhaps you read a different article to me, but where did the PM endorse a bigger bubble?

I did read him endorse more houses being built:

> Well I certainly think that it’s important to get more houses built and if there’s a strong market for flats and for houses, that’s a good thing, not a bad thing

Shut up and take my money!!!!

http://nationalhotspots.com.au/change-brisbane

Canadian Billionaire predicts the end of US dollar as worlds reserve currency:

http://www.youtube.com/watch?v=nX7J8-VTG08

My prediction is 2016 of major global financial collapse never before seen

@ Tim

I think reading between the lines ‘strong market’ means high demand which then equals high prices. The trouble is that the high demand is investor driven.

So once again the government won’t touch housing and the bubble will be allowed to run its course.

I’m actually all for the bubble now I hope it gets bigger to the point of absurdity. Only then we will get a significant correction and mindsets may change.

So bring on houses prices to the moon I say!

Don’t believe crazy boom theory

http://smh.domain.com.au/real-estate-news/dont-believe-crazy-boom-theory-20131003-2ux1n.html

@Average_Bloke

i cant agree more!

Average_Bloke, if only it were that simple! Several years ago, we would have said that the prices today are absurd, never thinking that they would actually get to these levels. I wish absurd levels would mean a significant correction, but the one thing we didn’t count on was the amount of money pouring in from foreign investors. It’s one thing to be subsidising local investors using their SMSFs to leverage into paying too much for property. But quite another thing to invite rich foreign investors to outbid Australians and then leave their properties empty!

I would have thought it absurd that the government favours speculators over would-be homebuyers just because they bid prices higher. How absurd that the government even promotes and then props up a bubble in the first place.

But inflating a bubble doesn’t necessarily mean it will pop. It should have popped years ago, but all my previous beliefs have all gone out the window now. The government will do whatever it takes to keep the bubble.

If it means only rich investors can buy, then so be it. If it means only rich Chinese can buy, they would rather that than let the bubble burst. If it means we have to fund negative gearers to the tune of $100 billion a year, then the government would do it gladly, and so would many taxpayers if it means their own properties go up in value.

So house prices to the moon? I’d say pop the bubble now if I had a choice. The sooner the better.

What a ridiculouly written article, and equally daft negative commentary from most people. Abbott said NOTHING wrong in this interview. He merely pointed out facts, and whether or not one wants housing prices to go up, depends 100% on which side of the fence you sit. Also The RBA acts indepentantly of the govt. Everyone seems to forget this point.

I am a home owner, and also have a few investment properties. I am not RICH, however I am prudent, and invest to get my family ahead. I WANT my assets to go up in value…….as would EVERYONE that owns a house or an investment property. Those that dont own a house or IP…..go and do what I did, and work your arse off to get one, and stop complaning about those that have done such.

@Paul and several others.

Yes, yes, sure we could jump on the housing wagon now, but YOU miss the point:

Housing exists for people to live in. Simple. By asking for prices to rise you effectively wish people to live sub standard lives or live in poverty.

I get that you want to increase wealth for your family. Any sensible human wants that.

But, the problem is, HOUSING/PROPERTY IS NOT A PRODUCTIVE INVESTMENT.

A productive investment, provides a better, cheaper, more efficient product to the public, while the investment owner, gains wealth through innovation and risk.

Google, became the library of the internet, so I don’t have to trawl page after to page find what I want. Efficient product for me, wealth for the owners. Ford built affordable transport, efficient product for me, wealth for the owners. THAT’S REAL INVESTMENT.

You guys who bang on about buying into property at any price have NO IDEA of economics at any level. Study history. An asset class, such as property, that has a fixed revenue base (ie. house prices can not over time rise faster than wages) will be subject to bubbles and cheap finance. But every time, throughout record history, regardless of political and fiscal manipulation,there will be at some stage a correction.

Now, I never expected property to do what it has. So I got caught outside of the market. But I’ve used the cycle to my benefit. Renting is cheaper, and more flexible, hell I’ve moved house 7 times in the last decade, and haven’t paid stamp duty once! I haven’t paid interest on any loan, no council rates, no insurance on an asset I don’t fully own, never paid for a plumber to fix a pipe…the list goes on and on. Each house has been better than the one before.

Now, compare my finances to my peers. They have interest repayments that consume their cashflow, they are barely touching the principal, but they believe they are rich because they don’t have a land lord.

Now check this out: By investing in PRODUCTIVE assets, we (wife and I) are now in a position where we have enough cash to purchase a GREAT place outright…debt free. In fact, the interest on our cash pays ALL our bills and rent.

So why haven’t we bought? Well, we’re in our 30’s, I have a growing business that could see us move interstate at some stage, she works for a government dept. that is in the midst of slashing budgets, so her employment isn’t 100% certain…Ah, gotta love flexibility.

Now, before you mouth off saying we must earn really well consider this: Between us our we don’t earn the “average Australian wage” for a couple. I just happen to be a 20/20 math student that sat down with a wise man when I was 20 and spent some time running through numbers.

And it’s really very simple when you step back from the whole property game: Why would any of the Australian banks (with billions and billions of dollars of resources) rather lend money to a bogan to purchase a property than purchase the property directly? The banks are monsters, their figures also tell them that over time property prices can’t out run wages, but a bogan will sacrifice everything rather than foreclose…which is the safer bet? A property that can rise in price at 3-5% per year (ie. wage growth) or a loan at 5-10% or more (secured against a property that can be sold?)? It’s soooo simple, sooo clear.

I admire any owner/principal residence. It’s a big move and I hope it works out well. But, those guys that have -ve geared IP after -vd geared IP, I have no sympathy when it goes bad:-and it will, you can not argue sanely against all recorded history.

Matty, you raise some great points, but have you factored in that the government will do ANYTHING to keep the bubble inflated? Read my post a couple of posts ago.

If interest rates were to rise, sure, many bogans (and others) would be in big trouble. They would have to sacrifice a lot to keep their property/ies or lose them. BUT what’s to stop a whole lot of investors and foreign investors from swooping in?

I get that house prices shouldn’t rise higher than wage growth, but the two parted company long ago. And to keep this phenomenon going, we have record immigration levels, unrestricted foreign investment, and now SMSF investors leveraging into property with the use of neg gearing.

The bigger the bubble, the more it consumes from the rest of the economy. I agree that it is unproductive, and it’s really an insane policy to keep inflating it. But that is exactly what’s happening.

Good on you for saving while renting. However, these days while rents are certainly much cheaper than mortgage repayments, rents are not cheap. In your case, you’re doing the right thing because you have already saved enough to buy if you wanted to. Whether you do buy or not, doesn’t matter because you can sleep well at night. What I am arguing is that government policies are encouraging a lot of stress – the stress of people not being able to buy a home, or the stress of those who have bought and are struggling, hoping that interest rates don’t rise from these historic lows.

Yes, the banks are monsters, but saying property prices can’t outrun wages – we’ve never had the level of foreign investment here bigger than we have now. There are more Chinese millionaires than there are Australians, and we can easily see how eager they are to get their money out of the hands of the Chinese government and park it right here. They’re buying new, second-hand, anything. They can easily get around our lax laws that aren’t even enforced anyway. And the government obviously doesn’t care that Australians are outbid by foreign investors, nor that they are outbid by local speculators. Maybe the bubble won’t pop for a very long time, defying logic and gravity.

@Paul of Brisbane – It’s no longer about “me, me & me” but about the future of the country. It sounds like you can’t see past your PPOR and your couple investment properties to see the unemployment rate increasing and business doing it tough. You might be “prudent”, but it doesn’t mean the entire economy is, nor is it sustainable.

@ Paul

Mate I’m all for you investing in property I just don’t want you or any other Negatively Geared property investor getting tax breaks at the tax payers expense. Getting tax breaks has nothing to do with hard work.

But I know that the government won’t change the status quo because investors like yourself would get upset and pull their vote next election.

Therefore I hope this boom really takes off and your house and ip’s triple in value or to the point where even people like you start to wonder whether property speculation is such a good idea.

@Paul,

You seem a little fearful to me, I hope for you and your family’s sake, your employment is 100% secure. Obviously, you must be worried because you wouldn’t be reading blogs on the state of the economy otherwise, one would think???

Best wishes to you but please keep your smug comments in check. Life has a funny way of turning on you when you least expect it 🙂

Oh @Paul, methinks thou dost protest too much.

Firstly, Tony Abbott is a cock and EVERYTHING he says should be taken with spurious malevolence at best and as downright neo-conservative bullshit at worst.

Secondly, I do work my arse off and I am very happy with my income level, but I would NEVER invest in property – it is a mug’s game for the lazy and the foolish. The maths DO NOT add up. Seriously man, investing in property makes no logical sense whatsoever. I’m not complaining about people like you, just people like you who leech off tax breaks like NG in order to make money for doing ABSOLUTELY NOTHING. This form of middle-class, tax-payer funded capitalism is disgusting – THAT is what we’re complaining about.

Thirdly, if you really think the RBA are not in cahoots with the government, you are a greater fool than I thought.

Look, I’ll give you some advice mate – sell your IPs NOW! There is a storm / crash coming and you should get out – NOW!!

Peace to you brother…

RBA independent???? Bwwwwwwwwwwwwaaaaaaaaaaaaaaahhhhhhhaaaaaaaaa. Mate I hope you’re a little better on the property research than your calls on RBA independence. His name doesn’t go down all that well here, but a lifelong property bull named Christopher Joye has been highly critical of the dovish politicisation of the board for the last two years and coming from him that’s saying something. I’d suggest you look him up, it might help with future decisions. In the meantime I’ve got a bridge to sell you, a little used, regular paint job……….!

debt goes up, poverty goes up, crime goes up.

your wife and kids safety goes down.

but you are still wealthy because your investments went up.

yeah….

@Rupert & Matty

so glad to see there are few smart people out there. i am not in the Mensa, but i do have an IQ of 146 and 3 Uni degrees, also i was in Mathematics Competitions when i was in high school. I’ve run the numbers a hundred times with my accountant friend, the number just do NOT add up.

me and my partner recently looking for a house to rent in Adelaide, from our understanding, things do not look good here.

we’ve been living in an 80s 3 bedrooms 7km from CBD house for a couple of year, the rent was and is $260(yeah its a house, and it does have a big front yard and a huge back yard). me and my partner will relocate our shop to a new shopping centre(a better location), we just wanna move closer to our shop.

anyhoo, we’ve been looking for a new or close to new house(or town house) with 3B2B2G, 7-8kms to CBD, 10mins to our shop to rent. guess what are the rental prices are – $340 to $380. FYI, a brand new medium house(or town house) within 7-8km to CBD here in Adelaide worth around $450,000, and we can rent it for just $340 to $380 a week. NO way am buying now, and good luck to the landlords.

there is another thing i would like to tell you guys, the rent here in Adelaide are dropping down for sure. there are simply way too much houses for rent(or sale) out there.

as i said we’ve been looking for houses to rent, and there was a favourite one we both fond of, which is brand new house with 3B2B2G, 6km to CBD, 10mins to our shop, 30 seconds to the main road, and 1 min to the shopping centre.

the agent asked for the price of $420 a couple months back. guess what, nobody applied for it. so the agent kept dropping the price down, finally it was down to $400/week. then we texted the agent said we can only pay for $370. the story ended up with that we got a great brand new house for only $380/week. no council fee, no water fee, no mowing, no plumber, no bank interests… i do feel bad for the landlord, hopefully he or she get most of it back from NG.

@paul

am hoping you do well over Brisbane. believe me or not, am not against property investment or NG what so ever, although i don’t own any house or IP(with our shop’s turn over, we sure can afford a house and a IP). however, i won’t do that you did, also i do work my arse off, thats why i won’t throw my hard earning money away.

I believe politicians should be held legally responsible for mismanagement of large amounts of money. Financial incompetence and corruption as seen as recently from Rudd and now continuing with Abbott should be punishable by law as they are based on personal and ideological decisions and not for the welfare of all Australians. Anyone for a call and collection of signatures to demand this? Spread the word!! DON’T BUY NOW!!

This is truly depressing. This is bigger than Australia and much larger than our property bubble. This goes to the very essence of human nature itself, and how our perception of reality is always reflected through the prism of self interest. We live in a world where we are running out of oil, the climate is changing, we plunder our resources and conflate debt with wealth. Yet the urgency of these things is denied. When you state these things as I have just done, you are branded alarmist or fanatical. But really…who are the fanatics….

Perhaps if people were educated about the vastness of the universe, the tiny spec which is our home, and the inconceivable amounts of time and luck that it took to evolve the rich pageant of life on this amazing planet and how this is being progressively eroded. I can already sense people’s eyes glazing over as they read this. They would sooner watch the rugby.

Carl Sagan said we were destined for the stars as a species, if only we could avoid killing each other first. If only we could all think big…bigger than ourselves and our tiny self interest. Please…let there be someone out there who gets what I’m saying.

http://www.news.com.au/business/breaking-news/bank-ceo-not-worried-about-property-bubble/story-e6frfkur-1226733645918

http://www.smh.com.au/business/the-economy/its-a-housing-boom-not-a-bubble-hsbc-20131008-2v5qn.html

http://www.smh.com.au/business/heres-how-the-housing-bubble-bursts-20130927-2uir8.html

Whatever this is, bubble or not… I just have this to say. I’m so happy I’m not a part of it.

Maybe I’m the only one who doesn’t believe there’s a pot of gold at the end of every rainbow…

@ Adam – I hear you brother and I totally get you. Very well put indeed!

@ Adam,

That comment of yours describes exactly how I feel about humanity at the moment…

@ Adam, never fear life on Earth will abide! It’s faced worse than us and pulled through. The only thing we are certainly screwing up is our own ability to live on it. Stupid monkeys – we won’t be missed.

Spruikonomics 101

http://newrulesforrealestate.com.au/

Warning you may throw up after seeing this.

@ Average_Bloke;

I only managed to go down about half way before my stomach couldn’t take it anymore. Jesus wept!

As for those population projections the more likely scenario, given all the growth-related predicaments facing humankind in the 21c, is probably closer to 2m by 2096.