The Australian has today reported on an emerging wave of subprime repossessions in Australia as times start to get tough.

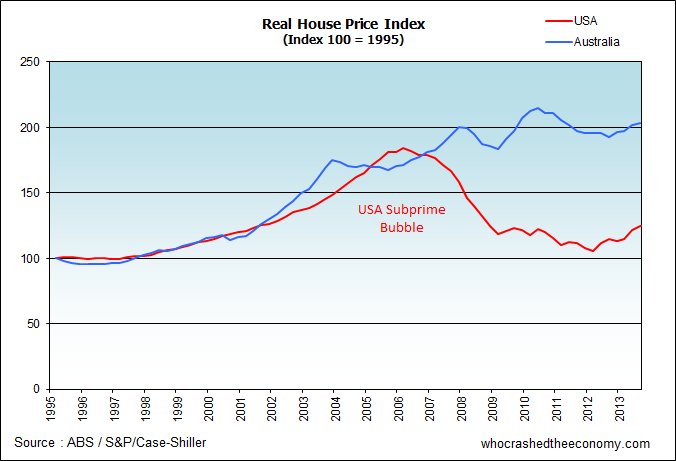

On Saturday, we reported how Australia has one of the largest property bubbles in the world, significantly larger than the USA subprime bubble. While evidence is emerging, our politicians are very much behind the bubble, you have to ask yourself, can Australia have such a large property bubble with prudent lending standards?

{kind=link}

“We have been in denial for years as a nation that we don’t have a subprime problem, but we do,” Ms Brailey, President of the Banking and Finance Consumers Support Association said.

The Australian reports on a Perth disability pensioner who was enticed to take out a $370,000 investment loan with a mortgage broker five years ago. After last year halting her payments, the loan has ballooned out to more than $1 million. Now the subprime lender has launched Supreme Court action to recover the property and the $1 million debt owing.

At 8:30am, ABC radio in Brisbane started a talkback show on Australia’s subprime mortgage crisis. The segment discussed how it is our major banks, who are writing[falsifying] most of these loans. As times start to get tough and the property market turns, people defaulting on their subprime loans has surged to three times normal levels. You can listen to the 15 minute segment, here.

And Tonight, the ABC’s 7:30 report has reported on alleged loan fraud by The Investor’s Club, now known as the Property Club. Mr McNally and Ms Mathews were enticed into buying four properties through the “free” club, and are now struggling to keep the family home after being forced to sell their business. They are suing The Investor’s Club after it was found the club’s broker has allegedly falsified loan application forms, grossly overstating income and providing loans they could not service.

The ABC said there are now four other TIC investors who have evidence of falsified loan application forms suggesting the practice is wide spread within the club. No doubt, many others could emerge tonight after the story has gone to air. Other TIC investors have also lost significant portions of their wealth investing in TIC properties such as Kirribilli Heights and now feel The Investors Club has mislead them. The ABC claims some properties have dramatically lost value and the projections of rental incomes have not been achieved.

» Pensioner represents tip of $100bn sub-prime iceberg: advocate – The Australian, 12th August 2014.

» Australia’s subprime mortgage crisis – The ABC, 12th August 2014.

» The Investors Club, renamed as Property Club, sued by couple claiming they were misled into taking out $1 million in loans – The ABC, 12th August 2014.

» The banks and the battlers’ bad loans – A Current Affair (Channel 9), 14th August 2014

& it’s not just property folks.

I now know several people who have lost vehicles in this low finance racket.

One commenter on this very site even has had a first hand experience where they were given loan/finance document pages disguised as the contract to buy.

These stories are only just the beginning. For every 1 person who gets air time, I bet there are hundreds who would never openly admit they have been done….Give it time and they will all come out of the wood work.

Another reason the trio of Abbott, Murdoch & Reinhardt want to put a gaging order on the ABC maybe? When will this mob be put away (or put down)?

https://www.getup.org.au/campaigns/media/ipa-abc-report/help-protect-ourabc-from-vested-interests-and-the-ipa?t=dXNlcmlkPTI0ODA0MzcsZW1haWxpZD01MzU3

Investor Club, LOL! You can find them in Martin Place during RBA meetings, protesting and holding placards warning them not to increase interest rates. Says it all.

As I’ve said before this is how the banks operate. In the late stages of a housing bubble the banks go after the savings and assets of those who simple cannot afford to service a loan. As long as the price that the asset is sold for after the default occurs is more than the value of the loan minus the deposit, the banks have still made a profit.

Of course if this is not the case, and most properties in default cannot be sold because of an illiquid market, (as it was in the US), the banks turn up on the door step of the federal government and demand a bailout.

Bankers will tell you that loans are a temporary transfer of wealth from the wealthy to the poor. It is clear that the intention of this sort of predatory lending is to do the opposite. Firstly buy snaffling up the savings of the poor and then by the creating a tax burden on the tax payers when the banks are bailed out.

Old news. The banks got done years ago for this practice. They destroy the loan application documents as soon as the loans approved. It’s common knowledge. I myself have shredded quite a few. You can then never prove it. We had one guy come in with an income of 50k get a loan for 600.

We put down he had no kids and it was classed as an investment property. Said his wife had a job and faked an income where it was his pay going into her account. Lol. Put him on a honeymoon rate just below std for a couple of years. We used something like $800 of his $850 after tax income. The house was some POS built in the 50’same that was falling apart. We valued the house at 550k but someone outbid him so he kept going.

Australians are property CRAZY. They have no idea what anything is worth lol. Keeps me employed. What’s cool is that if times are good I have work. When times are bad. I have work. Lol best job ever.

I’m not going to argue with people if they want to put themselves in that position. We’re just told to shred the papers once the loans approved. Poof. Then when they go under like they always do its like a 50% fold rate, we just claim the house. They always fold because they can’t afford food or bills or petrol then they split up. Who cares because then I have two people instead of one seeking more home loans haha.

You guys crying foul donot seem to understand. It’s a world of sharks out there. Get over it.

Why sugar coat it and call it a subprime loan? Why not call it what it is, MORTGAGE FRAUD! It is the targeting of assets owned by the financially naïve by the taxpayer protected banks. These loans are then securitised into Mortgage Backed Securities and sold to equally naïve institutions around the world with the compliance of fraudulent ratings agencies. Everybody knows it caused the start of the GFC so why let it continue? The solution is to take away the banks’ government protection and demand they show why they should not be broken up if they are shown to be insolvent.

You never have a sub-prime mortgage crisis until you do, and by then it’s too late… Sub-prime mortgages and loan fraud are just another way to get people’s money into the housing market that otherwise couldn’t afford it. It helps prop up the top-heavy market and it destroys lives.

Don’t let Nick Xenophon get away with his own legislative version of sub-prime loans: super for housing, sign the petition: http://t.co/Y8Y2kIKRLg

The RBA and Australian Government corrupt partnership and their policies of creating vast profits for a minority(banks,realestate, property spruikers, politicians)at the expense of the majority of all of us, thus risking Australia’s economic and social welfare is bordering on TREASON!! WAKE UP!! Australia.

The real answer is dismantle the RBA, let savers determine the interest rates, and have a sound currency.

This will happen, but only briefly as the elite will then convince the population that fiat, fractional reserve currency will make you wealthier…..Rinse, lather, repeat.

Rinse, lather, repeat.

It’s happened over 6,000 times. and Fiat currencies always collapse. The middle class get wiped out. The rich own everything. Then they preach the benefits of fiat currency, which the public buy, but in reality it steals from the working class every single day and benefits the rich. Rinse, lather, repeat.

@bilsabot

I have no doubt you’re doing what you say. Except, in this day and age, with social media and retrospective laws I would be very worried. If there’s no documents to prove the banks or it’s workers innocence then they are guilty by being negligent. The difference is the top management of the banks have lawyers you can never afford: The big boys wont see jail…but you little guys? There might not be a paper trail, but there would be an electronic trail that points to you as the issuing officer. If your being deceitful do you really think there is no risk? Why do you think loan officers aren’t on minimum wage? It’s danger money. But as a stereotype, you only care about your income. You might be laughing now, but nothings a one way ride. And this is becoming more and more evident: It only takes on p*#$%@d customer to find where you work/live. Is it worth it?

Just saying.

I guess what I’m say is that any authority that doesn’t keep a copy of documentation for financial transations that they have approved should be liable. Obviously our legal system is not up to the task of protecting consumers when disputes like this occur.

@bilsabot

I wonder how many laws are being broken in what you describe in your post.

APRA and the AFP would be most interested to make contact with you to discuss them further.

@bilsabot – do you work for Adelaide Bank / Bendigo? They shredded all their fraudulent LAFs a couple years ago.

@Matty – Most issuing officer’s are ghosts – especially within Westpac. Who you gonna call – ghost writers, of loans

When ASIC wouldn’t investigate, some people have gone to their local police station. When Detectives @ Tuggerah Lakes Police Station went investigating fraud at St George/Westpac, they found the loan officers don’t exist. They make up fake names for issuing officers of these fraudulent loans.

@Joshua

This maybe true. Ghost writers. Oh well, I guess they got away with it the………

I call BS on this. Where did the commission and bonus get paid to? It’s a task the authorities don’t wanna start, because we all know where it goes.

Just wait until there is a class action worth undertaking by the big law firms.

@Matty – you also have to wonder who has computer logins for the Westpac/St George Network – surely this is all logged. It would seem corruption goes deep in Australia – wonder if the police were paid off to say ghosts and provide a dead end?

Class action may be coming. Channel 9 news reported subprime along with the CBA profit tonight on the news. Tomorrow night, A current affair is running a story on four couples who have been subject to loan fraud and now have mortgages they can’t afford.

@Matty yeah that would be funny the big law firms going after the big banks. Very amusing.

I’m sure our property corrupt ministers would have the law changed accordingly to protect the banks. Banks are like no other institution or industry – too big to fail.

@bilsabot

You can tear up loan applications all you want. There will be a long trail of records and audit information in the back office systems! Ties back to land and property information systems (in Government) in terms of transactions (buy/sell) and a record of incumbency etc.

As for ‘loan officer ghosts’ if names are recorded in the back office and can’t be reconciled with HR records in the bank then we have a simple case of black and white fraud. I wouldn’t want to be the director of compliance.

Think Bilsabot makes a good point, hey he’s just sharing an insight from the inside. We should encourage more of this. Sounded a bit gloatish, but my gut and head both said it all adds up. And yes I just could be that simple and devilish.

I’m aware of several people/couples doing it it real tough, real tight. But hey! I was the idiot 5 years ago remember…

I’m seeing my income dry a little, because others are too. And shit is just getting more expensive.

Incoming!

https://www.youtube.com/watch?v=FsYSmvwnpQE

prepper

@Paul..

Sorry mate, blame the individual, if we live in an age where we can download Miley Cyrus, kids can damned well download the Australian Constitution if their brains permit.

What I need is Matty & Joshua to stand on a tall building in Sydney and shout…

“There might not be a paper trail, but there would be an electronic trail that points to you as the issuing officer”. And, “you also have to wonder who has computer logins for the Westpac/St George Network – surely this is all logged”.

I might not have a legal or financial background, but these observations would make me shit myself if I did and my bottom line depended on it.

Yes Patrick,

This is going to end badly for many.

I was interested in getting the word out that we can cast a no confidence vote at the next election and start a fresh

prepper

@Patrick

Sorry mate, I wont be doing that anytime soon. I like being anonymous for several reasons.

Not to blow my own trumpet, but while we have fiat currency I’m just not interested in making a scene, it’s just a waste of effort IMHO. I’m one those ‘idiot’ capitalist’s, who think governments should get outta the way:- School education and a fair level of health provided by the state, but beyond that, you’re on your own.

The trouble with a system like that is the wealthy elite can’t leave well enough alone, and then corrupt the system…Subsidies, tax meddling etc. etc.

And anyways, shouldn’t these ‘rogue’ loan officers know that the NSA can see what they are doing? lol Seriously, if any info is stored on any kind of network, you should assume it can be seen.

If the state can demand to access (physically/electrically) your home pc, imagine what a cranky lawyer will do when they see the opportunity of the largest class action payout in Australian history. Lol, talk about playing with fire. There are some weird laws around pc data, I wouldn’t feel too safe.

I think I’ve gone through 6 or 7 upstarts in the last 5 years filling in paperwork for me on the books 😉 Irish. Sean. Matt. Something or other… I can’t remember their names sorry. I don’t recall.

Additionally in 10 years no one. And I mean NO ONE has EVER questioned the branch I’m at. We’ve never been investigated we’ve never had them go over the forms. We can pretty much do anything we want 😀

The one guy we do know who got in trouble got a slap on the wrist. No fine no anything just a ‘go over your documents more throughly please’ haha. He was transfered to a different branch then when they came asking again we said oh he was fired from his branch. So they never looked again.

One elderly couple came in yesterday and took out a loan using their super for an investment property and wanted to fix the loan for 10 years but I managed to talk them out of it and got them on a variable lol. It was funny as. All I had to say was ‘this would be your repayment if rates went down and it was passed on in full’ I didn’t mention the fact that even if they do the most they will save is 25 points because our funding costs are already at the bottom. As opposed to the more likely event of them starting to go up in a few years haha. Also giving a 30 year loan to a pair of 70 year Olds. Gold. They have no idea what they are doing lol. How’s that my fault. They know the risks and they want to sacrifice all their income that’s not my problem. They already have 3 properties they can sell them if it goes belly up. Baby boomers are greedy. Their eyes light up when you tell them they can use their super to buy a other house. I only gave them product information. I didn’t tell them to use a variable rate simply explained to them how variable and fixed worked and why one might have advantage over another.

Seriously though you guys should understand it’s about making money not about what’s fair. I do feel bad for people under 30 they really are a generation of renters haha. I’m especially happy they have keep land release nice and slow and all the subsidies and tax concessions in place. I think they worked out they would use about 70% of their income on this loan so their super only paid them enough for food and bills. They could sell their other houses but they don’t way to and just want more and more houses. It’s not my problem people are greedy.

It is kinda crazy though my banks worth more than some of the big US banks with 1/10th the customers lol

Just thank my stars all my money and assets are overseas where it’s safe.

@bilsabot

Even psychopaths can be helped. Seek treatment immediately.

@22 Stop with the “haha”s and the “lol”s, you sound like a total c**t!

Yeah, he is sounding a bit like Joe Hockey. The fuel excise won’t hit the poor because they don’t drive, lol, haha.

Zero credibility.

@bilsabot

>Then when they go under like they always do its like a 50% >fold rate, we just claim the house.

And therein lies the flaw, eventually the house won’t be sold at a price to cover the loan. At which point the system will collapse.

As for your other claims (which I mostly don’t belive) for the simple reason why would anyone post such a confessional on the internet with a traceable IP?

bilsabot sounds like a real estate agent to me….

Real estate agents, bank loan officers basically come from the same cesspool.

@bilsabot you’re claiming to be some sort of loan shark that works for a big bank. Are you using a proxy when you post here? Your IP address date/time is logged with every post you make. This is enough information to determine your ISP and then obtain from them your real identity and in turn which bank you work for. I’m sure the CEO of your bank would love nothing more than the amount of bad PR you’re giving his bank and have to go into damage control to his shareholders and the general public because some low level putz at one of his hundreds of branches went online and mouthed off about how dodgy they are. Banks are constantly spending money on marketing to try and stop people from hating them. It’s funny how you claim that you will always be employed but your employer would fire you on the spot without a second thought over what you’ve been writing here.

Shamelessly stolen from MB forum:

Today’s Insiders is now up on iView:

http://iview.abc.net.au/programs/insiders/NC1476V029S00

Watch Tony Burke’s comments on negative gearing at 18:35.

Watch Gerard Henderson’s vigorous defence of negative gearing from 37:25.

Bilsabot is only being truthful, whoever they may be. He is only expressing what the Banks, Real estate industry, property spruikers etc. etc. see us as and that is the majority of us. We are so easily manipulated, persuaded, misled. The is easily proved by the fact that 80% of registered voters in Australia vote for the same Labor/Liberal-NP governing monopoly for many decades despite having proven themselves time after time how corrupt, incompetent and hypocritical they are. The Banks do not come to our door for business, we go to them. I believe we should reflect our behaviour above all first before we criticise anyone else. We should allow Bilsabot to feel free about commenting. He is only reminding us of what we the people do. We also live in a democracy.

@30 Yes, Theo, of course we should allow Bilsabot to feel free to comment. It doesn’t, however, excuse his conceited hubris about behaviour that is at best immoral and at worst illegal. So, after reflection, I remain very comfortable criticising him.

If what he says he has done is true, then he should be utterly ashamed of himself and be prepared to pay the consequences of his actions, should he have incriminated himself by broadcasting his contemptible and loathsome methods on this site.

Who knows – perhaps Bilsabot is the ‘smoking gun’ that is needed to kick-start some serious class actions against banks and policy makers.

I could not have said it better myself

http://wakeup-world.com/2014/07/19/understanding-the-illusion-of-money-and-the-economic-system/

prepper

You do know what bilsabot is doing isn’t illegal. Lending people money…. lol

Has anyone here actually gone and got a loan? It’s like buying a car…

They say anything to get you to borrow as much as possible then at the bottom of every for it says they aren’t financial planners…

Also you think coles and Woolworth feel bad about selling cigarettes? Something that physical kills someone vs something that just takes their money?

Might want to step back and take constructive feedback instead of just flaming it. This is why systems never get improved because as soon as someone sees someone else doing better than them in Australia they get hung up.

Also the banks got done for bum forms a couple of years ago already. The ere was a big ijvestigation into it and they found all forms had errors on them. Their punishment was exactly what he said. They were told to simply ‘check the forms’ that was it. So obviously it’s not something that in banking and lending that should be considered morally or legally wrong to the extent of say murder which is what you guys make it sound like.

Just my 2 cents.

@ 33. Jessjess, the reason systems never improve is because people are too selfish to look beyond their noses while lining their own pockets.

Just because something is lawful, doesn’t make it right. Guns are legal, but should they be? Cigarettes are legal, but should they be? At least those debates are on the table. The debate about the insidious practices of bankers and governments is never on the table, except on sites like this, so I will continue to fight for the cause of the honest man, of the kind man, of the decent man. I will work hard for my shekels, I will never be in debt, and believe you me, I could never be ‘hung up’ about an arrogant banker ‘doing better’ than me. I take the moral high-ground on that one my friend. He will never be ‘better’ than me!

Equity loans will be our Sub-prime Crisis.

Somewhere in 2015, 2016 or early 2017, external jolt bigger than 2008 seems to be highly likely. This, coupled with high unemployment and credit freeze when most are leveraged up-to nose. As a result, widespread fear and panic.

Any thoughts please?

http://www.businessspectator.com.au/article/2014/8/18/global-financial-crisis/world-must-inflate-or-bust-australia-mustnt-join

Treasury looks at negative gearing

http://www.abc.net.au/radionational/programs/drive/treasury-looks-at-scrapping-negative-gearing/5639474

Good link average_bloke. It makes sense given the issues the Abbott government is having with the budget. It will have to start targeting large ticket items and negative gearing is perfect.