The World’s Central Banks have today created countless financial bubbles through unconventional and unproven monetary policy.

Paralysed by the 2007/08 Global Financial Crisis (GFC) stemming from the burden of unsustainable debt levels, central banks and governments have tirelessly worked in unison to recklessly pump world economies full of more and more unproductive and destructive debt. Lengthy periods of emergency low interest rates and ballooning central bank balance sheets have accelerated growth in many of the very bubbles that abruptly brought the world to its knees in 2008.

A decade on, many wrongly assume the GFC is all but history – a crisis consigned to the history books. But in realty the 2008 crisis was just stage one, the warm up lap, of a much bigger financial crisis yet to rear its ugly head.

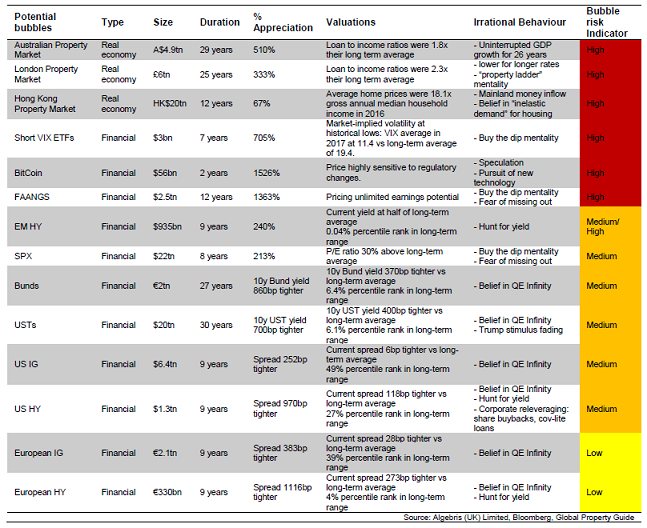

Algebris Investments have recently compiled a list of the world’s fourteen largest potential bubbles that exist today. They have been ranked by risk based on the size, duration, appreciation, valuation and evidence of irrational behavior.

Algebris’ Alberto Gallo remarked, “We’re in a world where most assets are overvalued, so in a world where almost everything looks like a bubble, the definition of a bubble has to be changed. You have to try to invest in the assets which look the least overvalued,”

He said it’s no longer just about valuations, but also irrational behavior. Gallo’s ten irrational “bubble” characteristics are:

1. “This time is different” – normal rules simply don’t apply.

2. “Fear of missing out” – get in, before you are priced out of the market forever.

3. “Sky is the limit” – the gains are limitless.

4. Flipping – speculators hoping for a quick profit.

5. “No credit, no problem” – bubbles normally form when credit is cheap and available, poor lending standards.

6. “Buy the dip” – Policymakers will be on hand to prop up the market, and bail it out. Policymakers won’t let the market fall.

7. “Borrow while you can” – rates are cheap, never a better time to buy.

8. “Bidding wars” – buyers fight for assets. Sydney property bubble anyone?

9. “The trend is your friend” – houses doubled over the last 7 years, so they will no doubt double over the next 7.

10. “Financial engineering” – derivative products to extract even more returns from the existing asset.

So where are today’s biggest financial bubbles?

According to Algebris analysis, Property Bubbles rank in first, second and third place as they are likely to inflict the most damage as most citizens require shelter.

Australia’s Property market is currently the world’s largest potential bubble having appreciated 510 per cent over 29 years. The London and Hong Kong Property Bubbles rank in second and third place.

Crytocurrency BitCoin comes in as the fifth largest potential bubble, followed by FAANGS – Facebook, Apple, Amazon, Netflix, and Alphabet’s Google.

» The Silver Bullet | Interplanetary Bubbles – Algebris Investments, 21st September 2017.

It’s somewhat an intellectual dishonesty to exaggerate that the Australian housing market is a singular market as many locations still have median prices under 400k on train lines ~ 20km from the CBD. Many places have had their bubble or still coming down, like mining towns and Perth. Just not where those facts get in the road of a good story.

“the everything bubble” indeed.

An interesting stat that has contributed to things been different here .

The population of Sydney in 2011 was 4 million today it is 6 million .

It took 230 years to reach 4 million and five short years to add another 2million .

Is having the most expensive real estate in the world really why people want to come here ?

Pardon my error above , 230 years should be 225 .

@Duncan – I think you are reading too much into it. As a global survey conducted by a UK firm, they probably only have financial aggregate data at a country level. For example, I can easily get household debt to household disposable income (or GDP) stats for Australia, but have never seen them just for Sydney or Melbourne.

Also the fact that Australia has multiple housing bubbles, means it makes sense to call it the Australian housing market. Have you ever seen reference to the “Toronto and Vancouver” property market. No, it’s always called the Canada Property Market.

Last, doesn’t the Perth suburb on a train line, 20km from the CBD share the same central bank and retail banks than the rest of Australia. So if the four big banks get into trouble over the high level of indebtedness, won’t all Australia be effected. Or do you have your own bank and economy that services your property on the train line, 20km from Perth?

It can’t be the everything bubble.

My wages sure aren’t in a bubble.

/sarcasm

Australia should be really referred to as a double sided bread warmer. Because most people are going to be toast.

What measures could we take to protect our assets? ie. invest in forex? foreign property market?

@Alex

The trick with bubbles, is it’s all in the buying: Never overpay for an asset. Sounds stupid when the market is rising hard, but the truth is overpaying for assets is dangerous: Remember how buffet was torn apart for missing the dot com boom? Who was left laughing after dot com bust????

And have minimal debt exposure: I have a feeling when it goes pear shaped, the banks wont be raising just one or two percent, I think it will be huge raises, will it happen in the short term? Dunno.

And always own stuff you can sell. If what you own is illiquid, when you need to exit most, you probably can’t, or you’ll take a huge hair cut.

@ Alex

Gold.

@ Alex

Even better than Gold. Invest in yourself (in whatever you deemed fit)

@Alex

With the new APRA emergency measures bill that The Treasury is currently trying to get through Parliament to allow banks to help themselves to private bank accounts I would suggest to only leave minimum funds in your accounts. Bitcoin is worth looking at with a 75% increase in a month and 15% increase for the last 7 days.

“(T)he Australian economy has grown through a property bubble inflating on top of a mining bubble, built on top of a commodities bubble, driven by a China bubble.

Unfortunately for Australia, that “lucky” free ride is just about to end.”

Australia’s Economy is a House of Cards

@Mercury

Thank you very much for that editiorial re: “Australia’s economy is a house of cards”, that was a great read, and a very accurate summation on the diabolical state of Australia’s economy.

Reading Australian Economy is a house of cards…. “Today 42% of all mortgages in Australia are interest only”

Glad to see the website has come back to life. This has been one of the few beams of light in dark darkness. Human wisdom is not ending with the many greedy liars sticking their tongues to every corner of the continent.

@duncan

Like max said, The problem is that everyone is basically under the big four, so once they start raising rates (due to overseas pressure), repossessing properties and fire selling them along with every over leveraged investor it doesn’t matter whether you’re in Melb Syd Perth broom or even in the farming sector.. the whole country has had land values blown out of the stratosphere due to cheap money and miss out mentality.

It’s going to all get very messy, we just don’t know how long..

‘the market can remain irrational longer than you can remain solvent’

The inevitable must be getting closer as the ECB is proposing the end of deposit protection. Bank Runs Anyone?

http://www.zerohedge.com/news/2017-11-19/ecb-proposes-end-deposit-protection

Well … this is my take on it. The housing think is only one small piece of a much bigger puzzle worthy of consideration here. Energy … Environment … Economics are intimately entwined and on shaking ground with too much of us humans to keep happy.

Any one of the 3E’s could trigger something quite nasty. If two or three tank at the same time we are in real trouble.

IMO … sooner or later there will be a depression from which there will be no short term recovery. House prices will continue to drop for years, maybe decades. There will be no recovery as such.

I mean really … is there any good solid news in any of the 3E’s these days?

A good time to get out of debt. Learn how to actually do something useful. Build community. Brush up on history. And relearn how to think. The ancients would have laughed at how dumb we have become with so much information at our finger tips.

Just an opinion of course.