Despite Australian’s love affair for residential property, Australia’s housing market might just be losing friends at a faster pace than facebook.

The latest loss is the Reserve Bank of Australia after governor Glenn Stevens said on Friday it should not “engineer a return to a housing price boom.”

Speaking in Adelaide to the American Chamber of Commerce (SA) AMCHAM Internode Business Lunch, Mr Stevens said he believed the household sector could be the reason behind such low levels of confidence especially after Wednesday’s ABS posting of a “quite respectable” 1.3% rise in GDP for the March quarter.

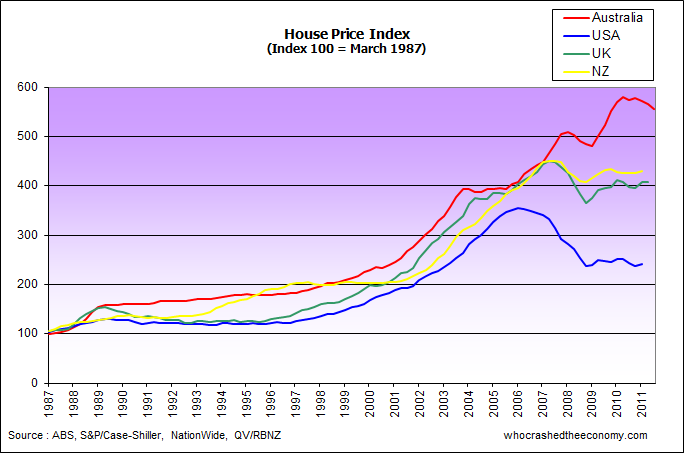

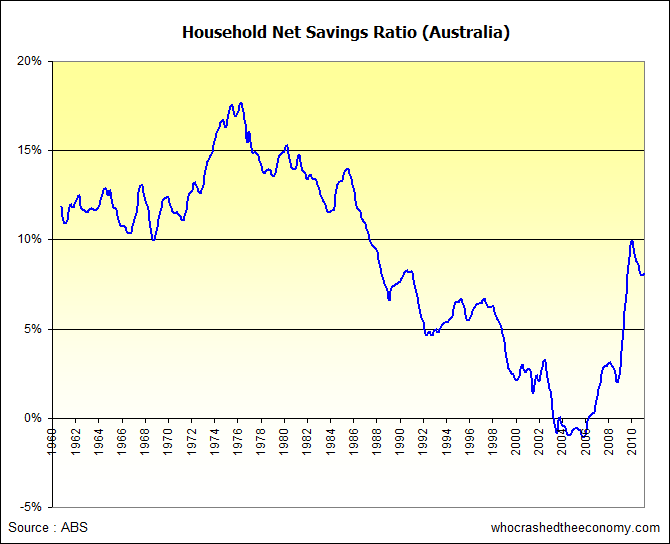

He described the decade or more leading up to 2007 as quite “unusual”. It was a decade when real asset prices (mostly residential housing) per person appreciated at 6 per cent or more per annum and household debt started to really pile up. The increase in perceived wealth caused household consumption to grow faster than incomes for a lengthy period and household savings to fall through the floor.

{kind=link}

{kind=link}

{kind=link}

Mr Stevens said Australia was not the only country to experience these trends, but avoided linking high household debt levels and years of irrational exuberance to the root cause of the GFC. He did note, however, that the GFC has reverted households back to more prudent and sustainable behaviour. Household net savings is now hovering around 10 per cent of household disposable income and household’s appetite towards leveraging for the purposes of asset speculation is waning.

Consumption is down and there is no surprise retailers are hurting with Mr Stevens saying “The gap between the current level of consumption and where it would have been had the previous trend continued is quite significant.”

However, ignoring the unusual and unsustainable boom period of last decade, current real consumption growth “is in fact, quite comparable with the kind of growth seen in the couple of decades leading up to 1995. It is in line with the quite respectable growth in income.”

For this reason, Stevens believes Australians should be happier than they currently are. But with fond memories of the boom times, Australians don’t see it that way. They want a return to these times, no matter how unsustainable they were, and there lies the problem.

“The decade or more up to about 2007 was unusual. It would be quite surprising, really, if the same trends – persistent strong increases in asset values, very strong growth in per capita consumption, increasing leverage, little or no saving from current income – were to re-emerge any time soon.”

House prices

Another area of dissatisfaction could be falling house prices. Real Estate agents have sold the expectation that house prices double every 7 to 10 years but as Mr Stevens points out – this is quite “unusual”.

Cuts to official interest rates in November and December last year, and a big 50 basis point cut in May has done nothing to help stabilise a declining market.

The RP Data-Riskmark Home Value index shows house price falls are picking up the pace, declining a further 1.4 per cent in May despite the 50 basis point cut. Melbourne led the falls with a 2.66 per cent drop for the month.

Earlier this week, data from SQM Research showed stock for sale on the market increased 2.4 per cent in May to 380,215 dwellings. In Melbourne, stock increased 7.6 per cent in the month.

On Tuesday, the RBA cut a further 25 basis points taking the cash target rate to 3.50 per cent. Many had expected another 50 basis points.

In addressing the implications for monetary policy, Mr Stevens said the RBA should not “engineer a return to a housing price boom” or “foster a renewed gearing up by households.”

Instead, we need the “right sort of confidence.”

“The kind of confidence based on nothing more than expectations of ever-increasing housing prices, with the associated willingness to continue increasing leverage, on the assumption that this is a sure way to wealth, would not be the right kind.”

Stevens also points out there is too much focus on the minority of the population – the just over a third of people who owns a mortgaged dwelling. The RBA cannot neglect those who live off their savings, adding “returns available to savers in deposits (with a little shopping around) remain well ahead of inflation, and have very low risk.”

Mr Steven’s speech could mean any future expectation of rate cuts is unlikely, barring any sharp external shocks to our economy. And when they do cut, they will make sure it won’t fuel our housing bubble. “As it happens, our judgement is that the risk of re-igniting a boom in borrowing and prices is not very high, and this was a key consideration in decisions to lower interest rates over the past eight months.”

» The Glass Half Full. Address to the American Chamber of Commerce (SA) AMCHAM Internode Business Lunch – The Reserve Bank of Australia, 8th June 2012

» More houses put up for sale – The Sydney Morning Herald, 5th June 2012.

» Housing market remains soft despite rate cuts – RP Data, 1st June 2012.

We are going to need a lot more than confidence and the ability to bank an extra 30 bucks a week to pull us out of our trillion dollar debt.

Mr Stevens said the RBA should not “engineer a return to a housing price boom”…

The key word being “engineer”.

Australians are still carrying way to much debt more than Americans per person. The only thing propping up Australia is mining and if China goes down the toilet then let see what Glen’s speech will be. I dont see rates going down for a few months but if all this data coming out proves to be BS then we will see more cuts.

I am glad he pointed out that only a third of the population have a mortgage. The focus in the media on the poor over-stretched home owners is sensationalist. What about the retirees and young people who are responsibly saving a deposit for a house, they always get forgotten.

What if the Government ‘engineers’ it instead. Still no changes to NG.

AverageBloke says “What if the Government ‘engineers’ it instead”

I don’t differentiate between the Labor, Liberal and the Reserve Bank.

I came around to figuring out that the Reserve Bank logo is the Triple Tau

of Royal Arch Freemasonry and a whole lot more that is inappropriate to discuss on this site.

This site provides great info on Australian house price trends.

LBS, if this is true, and I say if cause I haven’t confirmed it, then its not China propping up Australia. It is the massive debt-credit issuance that will ultimately bust us big.

http://www.australiandebtclock.com.au/

Speaking of China, does anyone know to what extent the average people (AverageBloke ;-D) of Australia are the beneficiaries China’s business with us? 17%? OK that’s one article I once read. How much goes off to foreign consortiums?

Also, if that debt figures at Australian Debt Clock are true, then Australia doesn’t own anything, not these resources, you don’t own anything with that much debt.

AverageBloke, Satan can come and rule Australia with a fireball fist, there would still be Negative Gearing here, its a mindset here nobody will dare touch, for better or for worse.

”The only thing propping up Australia is mining and if China goes down the toilet then let see–”

It is certain that at some time China will end its purchases of Oz ores.

China is buying huge amounts of iron ore from various places. , yet their demand is NOT commensurate with the volume and trype of products they are producing.

They of course say that they are having growth and need it for infrastructure , but when you compare how much they are buying and compare that to their growth and genuine need there is a great discrepancy.

So you do the math , why would a country be wanting to buy so much material, yet not seem to have a real need for that much volume. …. ?

While Ozzies may be anxious about the economy , that really is a small problem compared to what is really around the corner.

“What if the Government ‘engineers’ it instead. Still no changes to NG.”

You can’t engineer your way from under a truckload of debt…

“why would a country be wanting to buy so much material, yet not seem to have a real need for that much volume. …. ?”

To orchestrate the biggest ever stimulus package since the wheels fell off the world economy after the GFC…

Botrot,

Australian Private Debt is 2 Trillion and there are 21 million people divide that then Australian private debt it 95k per person in Australia

Total Debt in Australia everything govt, private etc is 3.9 Trillion and there are 21 million divide that then Australia debt per person is 185k per person

http://www.usdebtclock.org/

USD Private Debt 15 trillion and there are 300 million Americans divide that then American private debt is 50k per person

Total Debt in US everything govt private etc is 32 trillion and there are 300 million American divde that then American total debt is 100k per person.

Interesting if I have missed anything please correct.

Yes but the government can kick the can down the road like they have been for the past 10 yrs.

What I find interesting is that the media have jumped right behind Steven’s comments as though he’s a genius.

Comments such as:

“Wow, we were spending more than we earn? I had no idea”

“So, households are adjusting to spending less. That’s gotta be painful.”

“House prices tripling in ten years is an unrealistic proposal to repeat.”

“Rapidly rising house prices really hurt those trying to enter the market. It’s a bit selfish of home owners to want more price rises”

Are the general public really this stupid? Could they not see that refinancing your home time again and again, on the back of price rises, is spending money that you didn’t EARN?

Again, I repeat, look at Japan’s economic recovery since their burst in late 80’s/early 90’s. No one goes into debt (or small and manageable amounts) to purchase assets, homes, stocks etc.

Why is it that Australian’s will pay over $400,000 for a unit in the CBD of Adelaide, but in Japan they sell routinely for under $55,000? It’s all to do with the willingness to borrow. The Japanese got stung by debt issues (personally, their government debt is a grenade with a pulled pin) and are unwilling to borrow.

We will see a return to spending habits like that over the next 10 years.

Humans are massively emotional/psychological spenders. We (as a country) spent up on borrowed money (believing that we never had to consider repaying it: EQUITY MATE) but now that price deflation is gathering momentum we will see the wallets shut, the cards tucked away and we will save for those rainy days.

Hey, did anyone see that Japan’s stock market has hit a 28 YEAR LOW? That’s the result of the public being unwilling to borrow, to invest in assets and rather save money (or trade foreign markets as the Japanese do).

It’s like a time machine, to the open minded, whats going on in Australia has been seen before, many times around the globe.

G’Day LBS, no you haven’t missed anything. Australians always seem to be able to punch well above their weight.

Think the prudent and those that can run their lives at a profit, or even manage their finances (whether that would be debts or no debts), will be sunk on the same ship of fools?

Australia is in for a bigger under-class. Maybe just a few more people earning $300K+ p.a. but bigger under-class, smaller but wealthier middle-class, and a disgustingly rich aristocracy. Seems to be the way the World is heading. Maybe I got the the existence of a middle-class part wrong.

LBS

The scary thing about those population numbers is if you take out those under 18 and those over 65, you are left with a workforce of 15 million. From that 15 million take out the unemployed and government workers and you are left with 10 million to pay the bills and reduce our 2 trillion debt.