Boy, what a turbulent couple of weeks on global stock markets. In Australia, the All Ordinaries lost 3.75 percent over the week ending 29 July only to accelerate and plunge 7.49 percent the following week. This included a free fall of 4.21 percent last Friday. This week has seen some stability return the markets with a mild recovery of 1.70 percent.

Traders don’t appear to have a single clear reason as to why markets around the world started plunging. In Europe, it was feared the sovereign debt crisis would spread to Italy and Spain and with a potentially large European Union member country defaulting. These fears were worsened with EU parliaments going on August holidays and leaving only the European Central Bank on hand to provide bailouts.

In the United States Tuesday Week, Congress had approved an increase to the $14.3 trillion dollar debt ceiling, preventing an unprecedented default of U.S. debt. Under the plan, the debt ceiling would be increased by $2.4 trillion dollars while also cutting about $2.1 trillion in government spending over 10 years. It took a couple of days, but markets started to wonder if the cuts were in fact all it’s “cut” out to be and if ratings agencies would downgrade U.S. debt anyway.

Those fears were realised last Saturday morning, our time, when Standards and Poor’s took the unprecedented move and downgraded U.S. long term sovereign debt to AA+ explaining, among other things, that the $2.1 trillion in budget cuts “fell short” of the required $4 trillion it believed would be required to keep a triple A rating. Over the weekend, all and sundry went to the defence saying the downgrade didn’t really mean anything, but despite all the reassurances, the Dow Jones Industrial Average plunged 5.5 percent in trade on Monday.

At the peak of the turmoil this Tuesday morning, All Ordinaries index of the Australian Stock Market was down 24.4 percent from the high recorded on the 11th April. At close of trade today, the index is down 16.3% from the April highs.

All this rapid global volatility could be seen as the start of GFC2.

Back at home, both Treasurer Wayne Swan and Prime Minister Julia Gillard was trying to comfort Australians at a time when their super funds were evaporating in front of them. Both said the “Fundamentals” of the Australian Economy is strong, we have record low unemployment and low levels of public debt. There was no mention of Australia’s record levels of household debt. It was an eerily feeling, bringing back memories of Kevin Rudd during GFC1 saying “As Prime Minister I will not sit idly by and watch Australian households suffer the worst effects of a global crisis they did not create”.

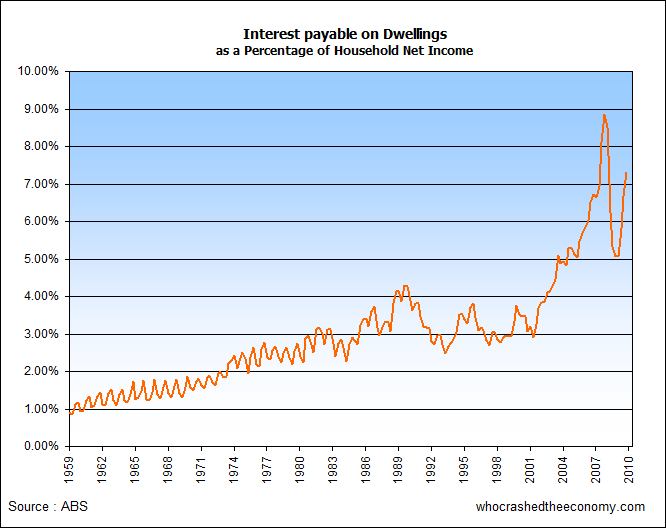

GFC1 was essentially about high levels of household debt around the world caused by speculation on housing and that lead to quite substantial housing and debt bubbles. The banks required credit growth and used financial engineering through Collateralised Debt Obligations (CDOs) and Credit Default Swaps (CDSs) to ‘protect’ themselves. When it all went wrong, Governments had to bail them out, effectively transferring the debt from private household balance sheets to the Government’s while at the same time trying in vain to stimulate unsustainable economies, creating surging public debts and sovereign debt problems.

In Australia in 2008, house prices were already starting to come of the boil after our own sizeable bubble. We had quadrupled household debt over a period of 30 years, with growth rates exceeding that of our United States counterparts. With so much money being soaked up in debt repayments, there was not much money left for retail and services underpinning jobs.

{kind=link}

{kind=link}

{kind=link}

Recessions are a normal part of the economic cycle. There will be a period where the economy will get ahead of itself followed by a slow down or correction. However today, Governments have decided we can’t have recessions or let markets run its course, instead we must prop up the economy as soon as it starts to look weak. 2008 was the perfect example, despite a local housing bubble and record levels of household debt, the Rudd government gave $900 handouts to prop up retail, and introduced very generous boosts to the First Home Owner Grants. This does nothing to address the underlying problems, namely our high levels of household debt.

As such, when the stimulus wears off, as it is doing now, we have found out that few can afford a home hence demand for housing credit is at all times low. Of those with a house and mortgage, they paid too much and now can’t afford to undertake discretionary spending, hence Retailing is now at the worst it has been in decades. If shops are not selling stuff, and builders not building homes then you could expect jobs will have to start going.

On Thursday, the ABS released job figures showing unemployment has risen to 5.1%. Economists are now forecasting unemployment will rise further in the coming months. On the same day, other data surfaced showing the number of companies placed into Administration has jumped 25% in June, the second highest monthly total on record.

It comes as a welcome relief today to hear Chris Evans, Minister for Tertiary Education, Skills, Jobs and Workplace Relations indicate the government has no plans for bailouts or new stimulus packages despite the fact that Australia’s economy is slowing and unemployment is trending up. Hopefully GFC2 wont trigger another knee jerk reaction from our Government to bailout unsustainable bubbles, effectively propping them up for another year or two.

» U.S. triple-A debt rating cut by Standard & Poor’s – 5th August 2011.

» More companies going to the wall – The Herald Sun, 13th August 2011.

» Government has no plan for new stimulus – Adelaide Now, 12th August 2011.

Thanks to reader, The_Mainlander for the title.

On top of all that, there are wage and salary reductions. That has been happening for the past few years too.

GFC2 is another phase (worsening) in the downturn, continuing from GFC1. Not the surprise phenomenon few politicians will present themselves slapping their dropped jaw faces claiming, “…now that was unexpected…”.

Up here in QLD the state govt has made available a $10k stimulus to purchase a ‘new’ home/unit. Sad thing is that it is available to Property Specufestors as well as struggling First Home Buyers. Once again another poorly thought out knee-jerk govt handout to keep the bubble on life support.

The thing is Average Bloke it aint working

I was only thinking the same thing eariler this week. Surely Julia was at any moment going to announce $1800 cash handouts to support retail while introducing a $28,000 first home buyers boost. Off course these measures were because of a failing global economy, and nothing we have created at home.

Although the pressure and lobbying on the RBA now to drop interest rates must be HUGE!

Problem is that the mentality hasn’t been purged. People think this is just a ‘blip’.

The second that interest rates go down, the masses will just load up on more and more debt.

And the banks will support them every inch of the way, knowing that they will get bailed out.

“preventing an unprecedented default of U.S. debt.”

No. Reaching a self-imposed limit on a credit card does not mean a person defaults on the credit card debt.

Yes, the inability of the US Government to continue to borrow to fund their deficits would have exposed the underlying depression conditions hidden by government spending.

I am curious……

This latest post has go me thinking about the whole “norm” now……

Do any of you get to the point where you actually get tired of all the negativity?

I mean like the endless whines of those who acted foolishly ( and greedily with housing ), the politicians acting like they had no idea, the miners complaining about extra taxation, the belief in perpetual growth, the belief in endless resources, the belief in endless welfare……… the disaster known as superannuation being feasted upon by fund mangers & financial planners.

It’s a freight train and you can’t stop it since it has been created by the majority, all you do is step out of the way.

Its clear now that 20th century thinking no longer applies in this country and if you want to succeed you need to adopt a new mentality and approach to life & money.

But I am just pondering after all.

I’m with you Romsey. I am thinking of putting a low offer on a house tomorrow for I am sick of waiting (and renting through a landlord who doesn’t believe in maintaining his property) and have a 60% deposit. The govt could push the bubble through policy for year to come. It has a large backyard which I can grow lots of food and wait out the next ten years. I can also paint it any colour I want!

The finance and real estate sectors are really starting to panic. This was just before the last RBA meeting.

Aussie John from Aussie home loans was on the radio saying along the lines that Australia’s different and the fundamentals are strong because of the coming mining boom and in the short term the RBA needs to cut interest rates to give consumers more confidence.

On the other hand on the same day the ANZ announced they would like to see an interest rate increase now because it could prevent 2 or 3 consecutive rises early next year which would be a disaster when price inflation really starts to kick in.

MissMoneyPenny if I had a 60% deposit I would be waiting on the side lines that deposit could quickly turn into an 80 or 90 % deposit over the next year.

Romsey, I know what you’re saying. I’m neither tired nor feel or see the world negatively. I’m capitvated by what is going on around me and the world. This “disaster known as superannuation” will increase to 12% if the Government gets its’ way. It is a good idea for people to put away for retirement, bad cause it will fuel those fund managers & financial planners.

Yes Romsey the freight train can’t be stopped, a lot of people (people I know quite well) have been hit by it. Can’t stop the freight train but you can side step it.

MissMoneyPenny, you’re not in the same league many others are in. You are in a very good position. In which case you should (opinion not instructive) consider engaging in any business, even property, exclusively on your terms and conditions. You are the one with the money.

20th century-industrial age thinking is over, and Romsey too right! One must think of new or different ways of acquiring an income/salary/wealth. The way I am seeing this is for starters, there is no distinction with work and life. Work now seems more like activities you get paid for, and these activities may occur anytime. That’s my situation and it can’t be like that for everybody due to the nature of their work I know. I wasn’t hit by the freight train so I am (fortuanately) in a position were I can think of suh activities. Also MissMoneyPenny, I’ll add you also have time on your side too. Bow to no one if you’re in such a postion.

The QLD Government has started it’s bubble stimulus with the 10k boost for First Home Buyers and poor suffering Tax Dodging Property Speculators.

http://youtu.be/3HhqeHuyw3w

More info from this Spruiker.

http://youtu.be/O7BsRKsSVu4

Warning these vids might make you vomit a little bit.

@MadMike

I have been waiting on the side line for 4 years. The offer hasn’t been accepted yet anyway…. If I see something suitable I will just offer low.

Dear Mr Romsey, I find your views interesting and wish to subscribe to your newsletter.

HT

MissMoneyPenny

Wouldn’t the 60% deposit if earning 6% at the bank pay most of the rent.

AverageBloke, I think its’ nigh time to figure out how, Trusts, Swiss Bank Accounts, Tax Havens, and Foreign Situs Trusts work, AND to see if you can get a CentreLink benefit on top of all that too (might as well go for a personal stimulus package while we’re at it). Here comes a very high Government debt to GDP ratio (on top of the enormous private debt).

That second vid, Crikey! I reckon being kidnapped and taken hostage is less scary, at lest your captors may feed you.

MissMoneyPenny I understand what you mean, there is a line in the sand with the satisfaction of living on one side and the math of economics on the other. There comes a point where you simply sicken of the whole scenario and you no longer want to wait for a further slide in house prices. You’ve got nothing to lose by making that offer is you’re happy with the price.

Four years is a long time to wait and there is no guarantee that the area you’re looking at buying in will fall the same as say another area elsewhere. We are not on this earth long enough to wait out everything and everyone, so you have to make a realistic decision on what will make you happy while you’re here.

I recently read in a financial book that it’s not how the economy of your country is going, but it’s how your personal economy is going…… if it’s going well then a recession is a great place to be since everything is on sale.

BotRot, I am so tired of the guilt card being played to me by the media now that I tend to ignore the hard luck stories, also I’m tired of charities and appeals, highway collectors, door to doors, and anything else I can’t think of right now. I also expected to cop it sweet after my previous post, but it appears that there is an agreement of sorts on my views, maybe I am not as twisted as I first thought. With respect to your last post about trusts etc, I do actually use a legal structure myself to invest, its part of my policy for fighting back against the growing band of leeches & robin hoods this country now has.

HousingTroll, I don’t actually produce a newsletter because I don’t have a financial planner license from the federal government that allows me to fleece you!!!!