Foreign investors in Australian real-estate will need to conduct their own sound due diligence after it has been revealed one of the countries leading house price indices has been overstating growth. But it is not the only problem they face.

Australia’s central bank has been forced to drop using a home price index from CoreLogic after the bank said it is “overstating” house price growth.

In a country obsessed with real estate, everyone used CoreLogic statistics as it always portrayed strong, perpetual growth regardless of actual market performance. The last monthly update, published on the 1st August found Adelaide dwellings surged a stunning 1.4 percent in the month of July. Sydney was up a hot 1.3 per cent and Melbourne 1.1 per cent. Corelogic boasted, “Capital city dwelling values reach a record high in July”

As of the 31st of July according to Corelogic, Sydney’s median dwelling price was $775,000 down from $780,000 the month earlier (yes down), Melbourne was $585,000 down from $587,500 a month earlier (yes down) and Adelaide was $417,500 down from $420,000 (no, no mistake – down). This on its own is not a concern. The Corelogic Home Value index is a Hedonic index meaning the data is “massaged” to better track attributes of the property – i.e. the number of bedrooms and bathrooms.

But it had become a regular occurrence this year. Month after month, median down, index up. Sydney started the year with a median $800,000 dwelling price and closed last month at $775,000 according to Corelogic. Despite the fall, Sydney has recorded impressive monthly growth, 0.5 per cent (Jan), 0.5 per cent (Feb), 1.0 per cent (Mar), 2.4 per cent (Apr), 3.1 per cent (May), 1.2 per cent (Jun), 1.3 per cent (Jul).

It is understood Corelogic made a “methodological change” in April and forgot to advise customers of the changes, including the Reserve Bank of Australia.

Apartment Boom

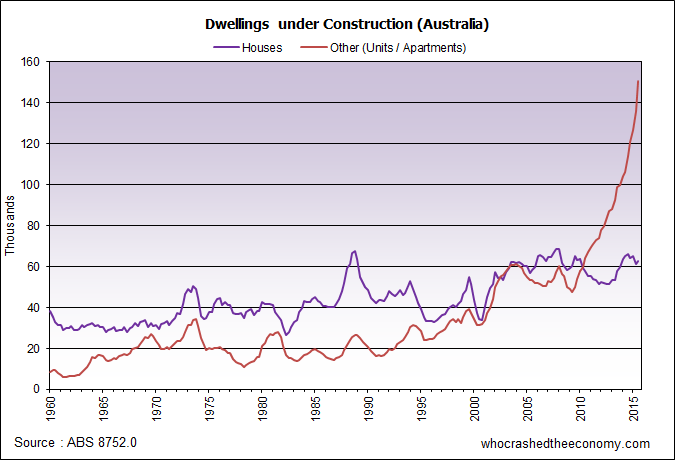

If you have been in Sydney, Melbourne or Brisbane of late, no doubt you would have witnessed the sight of endless cranes. Australia is in the grips of an unprecedented apartment building boom.

In the March quarter, according to the ABS, the private sector was building 150,706 “other” residential dwellings, typically units and apartments. This is triple the roughly 50,000 only 6 years ago.

Most of these dwellings are off-the-plan and are being built for foreigners. Investors put down, typically, a 10 per cent deposit and is required to pay the remainder when the apartment is complete. This could involve obtaining a loan with a bank when the time comes.

“All the deals have been frozen”

As we reported in May (Banks tighten screws on foreign buyers), Australia’s Big 4 had started retracting and clamping down on loans to foreign investors after detecting widespread fraud.

According to overseas mortgage brokers, many are now struggling to complete their purchases.

Mark Yin, an agent with Shanghai-based Home Tree Group told the AFR, “All the deals have been frozen,” According to the report, nearly 100 per cent of his clients were unable to get finance from Australian banks. Most were buying apartments in the Melbourne CBD.

“I have now stopped dealing in Australian property,” he said.

Lanny Xu, CEO of Iron Fish China said about 20 per cent of her clients were trying to on sell apartments after failing to obtain loans.

For local buyers, the oversupply of apartments have seen prices fall. Banks are valuing the apartment at settlement and many are coming up short. In Melbourne’s Docklands, CBD and Southbank, apartments are selling at up to 24 per cent discounts to the off-the-plan price.

According to a recent article in the AFR, off the plan apartment sales in Brisbane’s inner city is down 44 per cent in the last quarter. (Brisbane apartment sales collapse, settlements now key focus for developers)

» Brisbane apartment sales collapse, settlements now key focus for developers – The AFR, 10th August 2016.

» RBA says Melbourne, Brisbane apartment glut could increase settlement risk – The AFR, 5th August 2016.

» Surviving the off-the-plan finance crunch – The AFR, 28th July 2016.

» Frozen loans trigger Australian property funding crisis – The AFR, 25th July 2016.

» New apartment resale prices tumbling in Melbourne – The AFR, 27th May 2016.

» Risk and fear rise as failed apartment deals reach $5b – The AFR, 27th May 2016.

» Lender Firstmac adds to squeeze on apartment borrowing – The AFR, 27th May 2016.

» Receivers warn apartment developers to get ready on settlement risk – The AFR, 19th May 2016.

Great article. The stench of BS had been filling my nostrils in regards to CoreLogic. Results looked truly bizarre and out of step with a range of other data (housing finance, average loan sizes etc). Hope ASIC is looking at CoreLogic’s behaviour here as many honest people might have been fooled into buying.

“In Melbourne’s Docklands, CBD and Southbank, apartments are selling at up to 24 per cent discounts to the off-the-plan price.””

Isn’t it ridiculous I’m almost excited for this to happen, because it means I can pay the actual (real) price for something..I’m excited at the prospect of not paying a false price, when should someone be excited at an opportunity to pay what something is really worth?

A developer around the corner from me (Gold Coast) is trying to flog 2 + 2 apartments off the plans (boheme city village look it up yourself) from 460 k- 520 k , that’s $4-5000 p sq.m which is exactly what happened in the block in live in circa 2008…. onthehouse.com shows not one apartment has been sold since at a price above this, in fact apartment value now is still far less than most of the off the plan prices then.

Cheap credit, 20 k FHOG’s in we go, cross your fingers, dont look back…

@ Jamie

Not sure if FJOG & more cheap credit will cut it this time.Lots of people I know in their 30s & 40s have moved back with parents and are just waiting for things to change. Relying on bear capitulation & foreign funds to fill state gov’ts stamp duty coffers seems dangerous positions for gov’t to take.

I wonder when inflection point is reached wherein more money is being made by gov’t with property prices on the way down rather than up.

What is happening behind the scenes with the banks is way way way bigger than anyone is reporting.

@estupidos

Any more details?

I’m now waiting for 2-3 years to see how this plays out.

I may never buy a house, have no debt and would qualify for the fhog and would be able to buy one tomorrow if i wanted too.

I know a few who have bought of the plan – they all think they will get big bucks and be able to cover the mortgage.

Good luck I say!

@ James

I’m with you, how disheartening it is though to see capital growth outstrip savings.

I’ve researching some homes in my area, some have grown

back to back average compound growth of 8 – 10 % p.a for the last 10 years. Assuming average inflation of 2 % p.a , that’s 6 – 8 % p.a compounded real growth. Show me a bank willing to offer you that on your savings…the longer we wait the poorer we get, but like you I refuse to believe in it and lately it feels more risky like the scales are tipping. It will either stall or crash. Who knows what will happen if private lenders bail out those who cant get finance from the major banks here, it may even surge on for another decade.

These apartments are not being built for the youth of this nation. This is a global economy, multi-culturism and mass immigration is the new faith. Our recent history has become irrelevant. The 90 million CCP members are cashed up (ie: they don’t need debt). They will buy this place outright and “our children will become homeless in the country their predecessors built”. This is no accident it is called “changing the blood”. Look around it is happening before your very eyes. If you don’t see it you are living in denial. In 30 years this nation has gone from having the biggest middle class in the world (most affordable housing in the world , ie: price to income ratio) to the most indebted workers in the world . In this time frame housing has gone up nearly 10 times, in Sydney, yet average income has doubled , maybe or maybe not , depending on your luck or connection. Then when you factor in compound interest you realise the impossible task our children are up against. Greed is destroying the people of this beautiful land.

“Financials” comprise 45% of the All Ords index.

“Materials + Industrials” (ie: the real economy) is 22.5%.

Hmmm….

@9 James R

Yep, it’s a crazy circus. Seen what the bank of japan is doing over there??? https://mishtalk.com/2016/08/14/when-will-bank-of-japan-own-100-of-japanese-etfs/

It’s a scam: The whole world currency is sucking the life out of itself. Many, many people will be left owning NOTHING, but indebted to corporations, governments and the rich…. That wouldn’t be their plan all along would it?????

Either it’s co-incident or it’s planned. Only a fool could believe it’s all co-incident.

@flyingfox: Any more details?

May be bank losses leading to at least one major bank default?

That’s scary JamesR – to think our economy is 50% based on a non producing “asset”.

When this does pop will it be even worse than first thought?

Yes we are moving much closer to having a “FIRE” Economy based primarily on the Finance, Insurance, and Real Estate sectors. This is at the expense of a manufacturing and export-based economy.

When the shit hits the Fan it will be much worse than first thought. Unfortunately there aren’t many jobs left in the “Real or Productive Economy” therefore you will see unemployment increase significantly and the deck of cards will start falling.

It will happen, but when is the question? People have been saying the bubble will burst since 2005 and 11 years later nothing has happened.

There are too many vested interests to let this bubble burst, therefore they will delay this for as long as possible, possibly another few years!

An extra 71,600 part time jobs added to the economy whilst full time positions fall.

Give this one to a kindy kid to work out. Buisness has, it seems has no reason to hold onto a “productive asset”, lets trim the benifit so you can still make us money..just. Otherwise we have no choice.

It’ll turn into just..we had to let the part timers go.

That’s where the cards will fall in Australia.

@ Chippa… It’s been the longest speculation ever and given it hasn’t happened (yet) , complacency has built year on year (like the house prices) and there are no problems any more…

What’s more disturbing is the prospect of Private lenders filling the gap when the credit crunch happens and then we firm up for another few more years of the same shit backed by dropping rates and greedy banks adding fuel to the fire.. Shit is loose, I just got my 3rd pre approved credit card delivered to me in the mail….spend up peeps .. Care later.

The shit will hit the fan when the credit crunch happens and or consumption and unemployment come together

I work in the same building as these guys – all you ever hear them talk about in the lifts is the next big team outing or long boozy lunch…

@16 3S

Yes! My folks just went on a overseas trip of a life time: They were embarrassed to be seen on the same tour as the finance & accounting guys. The way they throw money around IS PROOF that it has never been earned through hard labour or justified by effort/risk/reward.

Pure plankton breed by private central bankers, fiat currencies, bought governments and a privately owned fractional reserve lending banking system.

I have no doubt of a full blown financial collapse/revolution in my lifetime.

Great article, Thank you so much. Have been following Core Logic as I try to buy a home and its gutted me into desperation thinking I must buy regardless and fearing more chinese buyers being brought in to ‘save’ the housing market.

Steve Keen has some great recent talks/lecures re the issue of private debt to GDP topping which is the sign we have been waiting for.

@Jamie

I am not sure if the Government has any more Rabbits to put out of their hat! Interest rates have almost hit Rock Bottom, House prices are higher than ever before, affordability is the worse it’s even been and our Private Dept is the highest in History…These Dipsticks at the RBA have no clue trying to encourage people into more Dept to borrow money they don’t have to buy things they don’t really need..good old Capitalism.

How long they can prolong the crash I don’t know, but they are running out of options fast. Unless there is another “Productive Boom” like the Mining Boom then the cards will start to fall no doubt.

We may not be in recession yet, but definately a period of stagnation and subdued growth for many years to come.

Vancouver housing market is IMPLODING….. down 20% in ONE month. The solution was to impose a 15% tax on Hot Chinese money laundering. If the banker’s PM wanted to control the bubble here he would follow their example.

http://www.zerohedge.com/news/2016-08-18/vancouver-housing-market-implodes-average-home-price-plunges-20-1-month-market-devas

Patrick @14, when they let all the part timers go there will not be enough full timers left to buy the goods on offer and the collapse will be even quicker.

The NSW purchase of trains from South Korea has been justified by being 25% cheaper than local manufactured ones. One claim is wages constitute around half the cost of building the trains, our wages are too high to justify local production.

So that’s around $1 billion wages lost to NSW and less steel from the steel mill they are trying to prop up.

Somehow I think the taxes paid on the wages, and company profits would be somewhere around the $500m mark, let alone the flow on benefits from keeping several thousand people in work and off benefits.

Can we offshore politicians jobs, language barrier is no problem as I don’t understand them now.

Check out the latest NSW average state transfer duty data. It shows that house price gains are picking up.

@ Chippa: The “FIRE” economy. So funny I had to laugh. But its so true. Now I’m going to cry. So many conflicting emotions.

This data is interesting, but there are other indicators our there, for example:

1. The real estate agent ‘celebrity factor’ index: which measures the number of photos of these guys on every street corner, newspaper…and generally the extent to which they believe they are gods.

2. The tradie earnings multiple: this index measures the total $$ earned by a tradie vs the average wage. This is currently running at about 500%.

3. % Financial sector of the All Ords. Currently running at 45%.

4. The ratio of the number of articles in the Sydney Morning Herald about young property guns on their 10th+ investment property vs articles about entrepreneurs who have started a real business. This is currently 10,000:1

Need I go on?

@23 JamesR

Real entrepreneurs in this country are few and far between: There’s a few of us having a go, but mostly we are just service industries, and we’re just cutting someone elses income down as we grow.

Real entrepreneurs, that grow GDP, increase our terms of trade don’t really exist. Cost of business, cost of labour, cost of resources etc. are just outrageous in this place.

Don’t let anyone tell you there will be a soft landing. That simply can not occur from here.

Check the media frenzy on this one

http://www.goldcoastbulletin.com.au/realestate/gold-coast-real-estate-palm-beach-homes-snapped-up-in-48-hours/news-story/dc64ba9b15f51b1737f5965c005e2da5

The current price of some houses in Palm Beach are up 30 – 50 % in 3 years.

@21. Well said Mark. Good point. Hit the current economy with a stick and it rings like a hollow drum.

i dont know what the big deal is,bankruptcies are a lot easier and faster now,i took my brother thru it because i had to show him on paper that he was working for nothing.its only 3 years now but i pity the fools who used their parents house as collateral for a loan

Just looking over the Auction Results, around Melbourne especially, does anybody know why they include sales that occurred days, or even weeks before in that auction day result?

For example for the 27/08/16 Auction Results, there are over 800 auction reported in the results, however more than half of them are from sales that occurred much before that date.

Anyone know if this is them doctoring the results to make them look inflated, or is it just the way it has always been done?

Cheers.

@ 28 Damian

IMHO, don’t waste time reading/searching/watching ANY of these figures. Auction reports have clearly been ‘seasonalised’ for at least the last 10 years.

What’s important is there is a bubble: Don’t get sucked into it with massive amounts of debt: If you need to buy, then do so, but don’t throw away the next 40 years of your life to a loan on a ‘security’ that’s way above what it should be.

36% of Australian pensioners living in poverty . Oz ranked 31 from 32 OECD nations .

Latest from MSM is trying to scare people by saying first home owners now need their parents to buy a house for them and pointing out Sydney prices. No explanation for price drops in Perth despite continuing low interest rates.

Maybe prices have dropped in Perth because iron ore used to be $150 and now it’s $30.

A timeless quote which really sums up our current banking and political system.

“You may know society is doomed when you see that in order to produce, you need to obtain permission from men who produce nothing; when you see that money is flowing to those who deal, not in goods, but in favors; when you see that men get richer by graft and by pull than by work, and your laws don’t protect you against them, but protect them against you; [and] when you see corruption being rewarded and honesty becoming a self-sacrifice.”

-Ayn Rand, “Atlas Shrugged”, 1957

Yes property prices have gone beyond crazy in Sydney and a few other cities . But in the rest of the country they have actually gone down in real terms . 30 years ago (one hour from Sydney) a house cost $160,000 . Today similar houses cost $320,000 . The land value , three decades ago, was $25,000 . These days the land purchase price is $200,000 . Therefore , we can see that in 1986 it cost approx. $135,000 to build a house (labour and materials) with no profit . In 2016 (when you deduct land value from house purchase price) we see that the house is being built for $120,000 (labour and materials) . Builders and “tradies” are much worse of than they were in 1986 The only people benefiting from this are the FIRE industries and their connected mates . Please prove me incorrect . Even at these low prices , it still takes decades to pay of a family home .

@ 56

Talking of connected mates, I had to laugh at the Banker’s PM speech to the G20 where he says “We need to civilise capitalism” Obviously Crony Capitalism is not enough for the political elite they need to own it all and completely shut out the uncivilised productive class.

http://www.zerohedge.com/news/2016-09-06/australias-prime-minister-ex-goldman-banker-warns-g20-civilize-capitalism

@56. You are dreaming mate as I don’t know what suburbs you’re looking at for $320,000, as places 1hour away like Wollongong, Gosford, Penrith are all $600K+ for a stock standard house.

Even crappy suburbs around Campbelltown and Minto are fetching over $500K.

Trust me the tradies, especially skilled tradies like plumbers and sparkies are making a killing and have been for the past 15 years.

Chippa , pardon me for not being up to date . I only just realised that land has risen 50 to 100% in the past 12 months . What is causing this dramatic rise ? The figures I gave above , were not for brand new 4 bed houses , but for typical 2 and 3 bed second hand houses (approx. just over an hour away). When we factor in , land price increase this year , we can see that our figures may be meeting somewhere in the middle . Maybe plumbers charge more in metro suburbs of Sydney , but most trades like carpenters , plasteres , painters are lucky to be making $30 per hour if working on contract beyond east.subs , inner west , north shore and beaches . Do you think a skilled carpenter ( the builders builder) deserves $50 per hour these days ? Please remember the craftsmans business investments that are vehicle tools maintainence insurances taxes . Deduct these operating costs from hourly rate you may realise that a babysitter probably makes more than these hard workers .

I forgot to mention the downside of being a worker in the building industry . That is the constant exposure to poisonous composite “sustainable” building materials . A deregulated wild west in the system of “civilised capitalism” . The timber yards have gone and so has the timber . That’s why everything is painted gloss white with poo underneath .

@56

Comment #30 “36% of Australian pensioners living in poverty .”

Thats really just their fault for not planning for their retirement. You know, epople who blow all their money and “live like there is no tomorrow”.

Comment #34 “30 years ago (one hour from Sydney) a house cost $160,000 . Today similar houses cost $320,000”

False. Today cost of building a 20 square house is $180k+. 12 years ago was $125K. 30 years ago it would have been much less the $160K you claim.

Lets keep things in perspective.

@56. Points taken…Unfortunately a tradie or any other service job needs to charge very high hourly rate because the cost of doing BUSINESS in Austtralia is ridiculous.

A family member of mine is a mechanic earning $21.50 per hour Gross, yet the company is charging his services to the public for $90.00 per hour, why?

The general public would think, that’s a rip off, but when you factor in the cost of Huge Rents, Payroll tax, public liability insurance, workers comp, superannuation, bank account fees, company taxes, quality assurance, safety costs, and so forth then cost seems justified.

Everybody want’s their cut and then the costs blow out of proportion.

This is part of the reason Australia is not competitive.

Apparently the apartment market will crash in 6 weeks due to banks shutting off financing to Chinese buyers, according to a US security think tank. The story becomes interesting when they claim it will stifle production of our new Sub Fleet. Read on …

http://www.news.com.au/finance/economy/australian-economy/australia-six-weeks-from-a-housing-collapse-us-report-warns/news-story/866d2fdee41b1227ce654f66ed8d9837#itm=newscomau%7Cfinance%7Cnca-finance-plmnt-trending%7C1%7Csection-finance%7Cindex%7Cmarkets&itmt=1473727703879